Study: New Federal Tax Law Would Exacerbate Economic Damage of Prop 80

This report earned media coverage on WGBH radio, WBZ radio, and Fox 25 TV, Bloomberg radio; The Boston Globe, the Associated Press, MassLive/The Springfield Republican, Newburyport News, Gloucester Times, Salem News, Lawrence Eagle-Tribune, Greenfield Recorder, CommonWealth magazine, and The Lowell Sun.

Cap on state and local tax deductions to hit Massachusetts hard

BOSTON – Recent passage of the federal tax overhaul legislation will exacerbate the negative economic impact of Proposition 80, the proposed constitutional amendment scheduled to appear on Massachusetts’ November ballot that would add a 4 percent surtax on annual taxable income over $1 million, according to a new study published by Pioneer Institute.

“The combined effect of Proposition 80 and the Tax Cuts and Jobs Act’s $10,000 limit on deductions for state and local taxes will double the Commonwealth’s effective state tax rate for high-income taxpayers,” said Pioneer Executive Director Jim Stergios. “That is not a good calling card for Massachusetts.”

Pioneer Institute’s analysis of data promulgated by the Internal Revenue Service on components of federal tax returns filed by Massachusetts taxpayers demonstrates that the average amount of state income tax paid by a taxpayer with a taxable income greater than $1 million would more than double (after adjustment for the decreased value of the federal tax itemized deduction) from $153,152 to $318,095.

The proposed constitutional amendment would make Massachusetts’ top marginal income tax rate the nation’s fifth highest.

Practically speaking, the Commonwealth’s top marginal income tax rate would likely rank even higher than fifth if Proposition 80 is adopted, because Massachusetts doesn’t allow deductions for a number of expenses, including home mortgage interest, and limits other deductions such as employees’ contributions to pension plans, that are allowed in California, Maine, Iowa, and Minnesota – the four states with the highest income tax rates.

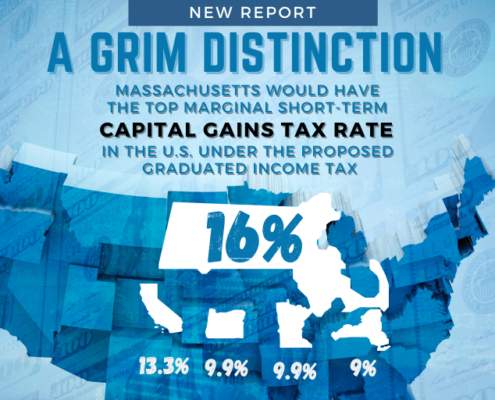

Massachusetts is also the only state that has a separate, higher tax rate for gains realized from the sale of securities within a year of purchase. If Proposition 80 is adopted, that rate would rise to 16 percent, highest in the nation.

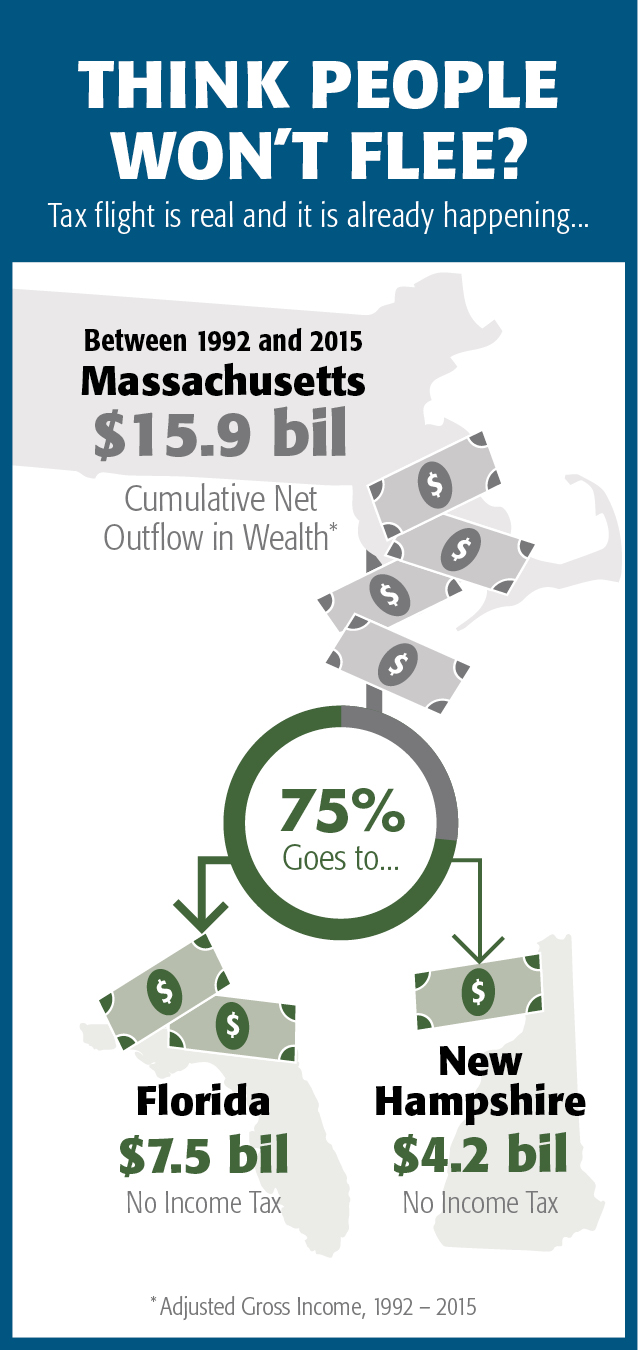

Nationally, the eight states with no income tax saw an in-migration of about $65 billion in adjusted gross income (AGI) between 2011-12 and 2014-15. The eight states with the highest income tax rates saw an out-migration of more than $44 billion over that period.

Between 1992-93 and 2014-15, Massachusetts had a net outflow of $15.9 billion in AGI. Nearly three quarters went to Florida and New Hampshire, both of which have no state income tax.

Every taxpayer whose AGI is in the top one-thousandth of 1 percent who leaves Massachusetts for a state with no income tax would save – and the Commonwealth would lose – about $13.5 million annually.

“The idea that Proposition 80 will generate free money for the Commonwealth with no down side flies in the face of evidence from Massachusetts,” said Pioneer Executive Director Jim Stergios. “Over the past two decades, the net outflow of wealth to Florida and New Hampshire has already been pronounced. Passage of Proposition 80 will speed the exodus of wealth from Massachusetts and could turn the Commonwealth into Connecticut, with stagnant revenues and a reputation for being unfriendly to business.”

Click on image to view full graphic:

About Pioneer

Pioneer Institute is an independent, non-partisan, privately funded research organization that seeks to improve the quality of life in Massachusetts through civic discourse and intellectually rigorous, data-driven public policy solutions based on free market principles, individual liberty and responsibility, and the ideal of effective, limited and accountable government.

Get Updates on Our Economic Opportunity Research

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-02-08 06:15:472022-02-08 06:15:47Study Finds Bus Rapid Transit Can Offer Cost-Effective Benefits

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-02-08 06:15:472022-02-08 06:15:47Study Finds Bus Rapid Transit Can Offer Cost-Effective Benefits https://pioneerinstitute.org/wp-content/uploads/public-statement-1.png

900

1600

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-27 11:57:102022-01-28 11:24:17Pioneer Supports Legal Challenge to Misleading Tax Ballot Language, Releases Video

https://pioneerinstitute.org/wp-content/uploads/public-statement-1.png

900

1600

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-27 11:57:102022-01-28 11:24:17Pioneer Supports Legal Challenge to Misleading Tax Ballot Language, Releases Video https://pioneerinstitute.org/wp-content/uploads/FareEvasionWeb.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-19 06:09:272022-01-19 08:40:42Study Raises Concern That Annual T Fare Evasion Costs Could Rise By More Than $30 Million Under AFC 2.0

https://pioneerinstitute.org/wp-content/uploads/FareEvasionWeb.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-19 06:09:272022-01-19 08:40:42Study Raises Concern That Annual T Fare Evasion Costs Could Rise By More Than $30 Million Under AFC 2.0 https://pioneerinstitute.org/wp-content/uploads/Understatement-web-post.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-18 06:52:502022-01-18 06:58:42Study: Tax Up For A Vote In November Would Ensnare Over Three Times More Taxpayers Than Previously Estimated

https://pioneerinstitute.org/wp-content/uploads/Understatement-web-post.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-18 06:52:502022-01-18 06:58:42Study: Tax Up For A Vote In November Would Ensnare Over Three Times More Taxpayers Than Previously Estimated https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-19 10:49:272021-11-19 10:49:27Public Statement on Massachusetts High Technology Council’s Challenge to the Graduated Income Tax Ballot Language

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-19 10:49:272021-11-19 10:49:27Public Statement on Massachusetts High Technology Council’s Challenge to the Graduated Income Tax Ballot Language https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-17 05:55:222021-11-17 05:55:22Study: “Millionaire’s Tax” Would Have Far-Reaching Effects on “Pass-Through” Businesses

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-17 05:55:222021-11-17 05:55:22Study: “Millionaire’s Tax” Would Have Far-Reaching Effects on “Pass-Through” Businesses https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-10-07 06:00:242021-10-07 06:00:24Study Warns that New Hampshire Tax Policies Would Exacerbate Impacts of a Graduated Income Tax

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-10-07 06:00:242021-10-07 06:00:24Study Warns that New Hampshire Tax Policies Would Exacerbate Impacts of a Graduated Income Tax https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-11-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-09-27 05:54:502021-09-27 05:54:50Study Finds SALT Deduction Cap, Graduated Income Tax Will Combine to More Than Double Tax Burden on Some Households

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-11-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-09-27 05:54:502021-09-27 05:54:50Study Finds SALT Deduction Cap, Graduated Income Tax Will Combine to More Than Double Tax Burden on Some Households https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-1-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-08-10 05:39:222021-08-10 05:39:22Study Suggests How to Advance Fairness, Predictability of “Payment in Lieu of Taxes” Programs Aimed at Nonprofits

https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-1-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-08-10 05:39:222021-08-10 05:39:22Study Suggests How to Advance Fairness, Predictability of “Payment in Lieu of Taxes” Programs Aimed at Nonprofits https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-23.png

512

1024

Pioneer Institute

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Pioneer Institute2021-08-05 07:52:132021-08-05 07:54:42Public Statement on Implementation of the Charitable Giving Deduction

https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-23.png

512

1024

Pioneer Institute

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Pioneer Institute2021-08-05 07:52:132021-08-05 07:54:42Public Statement on Implementation of the Charitable Giving Deduction https://pioneerinstitute.org/wp-content/uploads/Tax-Flight-Photo-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-17 05:26:022021-06-17 09:24:04Study Says Massachusetts Surtax Proposal Could Reduce Taxable Income in the State by Over $2 Billion

https://pioneerinstitute.org/wp-content/uploads/Tax-Flight-Photo-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-17 05:26:022021-06-17 09:24:04Study Says Massachusetts Surtax Proposal Could Reduce Taxable Income in the State by Over $2 Billion https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-09 09:29:102021-06-09 09:29:10This Is No Time for a Tax Increase

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-09 09:29:102021-06-09 09:29:10This Is No Time for a Tax Increase https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-01 05:54:112021-06-01 05:54:11Study Finds Deep Flaws in Advocates’ Claims that the Massachusetts Tax Code is Regressive

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-01 05:54:112021-06-01 05:54:11Study Finds Deep Flaws in Advocates’ Claims that the Massachusetts Tax Code is Regressive https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-05-05 05:33:362021-05-05 06:04:38Study Says Interstate Tax Competition, Relocation Subsidies Exacerbate Telecommuting Trends

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-05-05 05:33:362021-05-05 06:04:38Study Says Interstate Tax Competition, Relocation Subsidies Exacerbate Telecommuting Trends https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-6.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-28 15:02:212021-05-10 14:19:147 Reasons to Reject the Graduated Tax and Instead Focus on Growing Jobs

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-6.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-28 15:02:212021-05-10 14:19:147 Reasons to Reject the Graduated Tax and Instead Focus on Growing Jobs https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-26 05:08:592021-04-26 05:22:50Study Warns Massachusetts Tax Proposal Would Deter Investment, Stifling the “Innovation Economy”

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-26 05:08:592021-04-26 05:22:50Study Warns Massachusetts Tax Proposal Would Deter Investment, Stifling the “Innovation Economy” https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-20 05:46:542021-04-20 15:51:32Study Shows the Adverse Effects of Graduated Income Tax Proposal on Small Businesses

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-20 05:46:542021-04-20 15:51:32Study Shows the Adverse Effects of Graduated Income Tax Proposal on Small Businesses