Tag Archive for: tax

https://pioneerinstitute.org/wp-content/uploads/MBTA-Subway-Returns-Feature.jpg

450

600

Eamon McCarthy Earls

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eamon McCarthy Earls2019-04-01 16:48:532021-10-29 15:18:12MBTAAnalysis: A look inside the MBTA

https://pioneerinstitute.org/wp-content/uploads/MBTA-Subway-Returns-Feature.jpg

450

600

Eamon McCarthy Earls

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eamon McCarthy Earls2019-04-01 16:48:532021-10-29 15:18:12MBTAAnalysis: A look inside the MBTA https://pioneerinstitute.org/wp-content/uploads/CloseupClock-1.jpg

739

1244

Mary Connaughton

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Mary Connaughton2017-02-20 12:34:192017-02-21 09:47:58The Clock is Ticking…….

https://pioneerinstitute.org/wp-content/uploads/CloseupClock-1.jpg

739

1244

Mary Connaughton

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Mary Connaughton2017-02-20 12:34:192017-02-21 09:47:58The Clock is Ticking……. https://pioneerinstitute.org/wp-content/uploads/SW-Launch-EBH-3-502x162-1.jpg

162

502

Teddy Wynn

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Teddy Wynn2023-06-22 12:42:192023-06-22 12:42:19Online Sports Betting as a Form of Tax Revenue

https://pioneerinstitute.org/wp-content/uploads/SW-Launch-EBH-3-502x162-1.jpg

162

502

Teddy Wynn

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Teddy Wynn2023-06-22 12:42:192023-06-22 12:42:19Online Sports Betting as a Form of Tax Revenue https://pioneerinstitute.org/wp-content/uploads/Copy-of-Hubwonk-Template-1-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-25 10:51:452023-04-25 11:10:56Losing Talent and Treasure: Uncompetitive Tax Regime Drives Upper-Income Exodus

https://pioneerinstitute.org/wp-content/uploads/Copy-of-Hubwonk-Template-1-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-25 10:51:452023-04-25 11:10:56Losing Talent and Treasure: Uncompetitive Tax Regime Drives Upper-Income Exodus https://pioneerinstitute.org/wp-content/uploads/Hubwonk-Template-98.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-11-01 09:48:452022-11-01 09:51:39Grading State Governors: Do Higher Taxes Equate To Higher Value?

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-Template-98.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-11-01 09:48:452022-11-01 09:51:39Grading State Governors: Do Higher Taxes Equate To Higher Value? https://pioneerinstitute.org/wp-content/uploads/video2.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-10-13 15:51:192022-10-13 15:55:45How did tax hikes work out for Connecticut?

https://pioneerinstitute.org/wp-content/uploads/video2.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-10-13 15:51:192022-10-13 15:55:45How did tax hikes work out for Connecticut? https://pioneerinstitute.org/wp-content/uploads/WSJ-web.png

512

1024

Jim Stergios

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Jim Stergios2022-09-09 17:20:182022-09-09 17:20:18WSJ op-ed: Don’t Make Massachusetts ‘Taxachusetts’ Again

https://pioneerinstitute.org/wp-content/uploads/WSJ-web.png

512

1024

Jim Stergios

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Jim Stergios2022-09-09 17:20:182022-09-09 17:20:18WSJ op-ed: Don’t Make Massachusetts ‘Taxachusetts’ Again https://pioneerinstitute.org/wp-content/uploads/Hubwonk-Template-89.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-08-23 09:49:202022-08-23 09:49:20The Taxman Cometh: Who Will Pay When the Newly Funded IRS Knocks?

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-Template-89.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-08-23 09:49:202022-08-23 09:49:20The Taxman Cometh: Who Will Pay When the Newly Funded IRS Knocks? https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-29 11:28:502022-07-29 11:28:50Pioneer Institute Expects That Massachusetts Taxpayers Will Be Refunded $3.2B Due To State Revenue Cap

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-29 11:28:502022-07-29 11:28:50Pioneer Institute Expects That Massachusetts Taxpayers Will Be Refunded $3.2B Due To State Revenue Cap https://pioneerinstitute.org/wp-content/uploads/Blog07-Cover.jpg

630

1200

Joseph Staruski

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Joseph Staruski2022-07-19 07:40:552022-07-19 07:41:50New Report: Massachusetts Maintains Reasonable Debt Relative to GSP

https://pioneerinstitute.org/wp-content/uploads/Blog07-Cover.jpg

630

1200

Joseph Staruski

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Joseph Staruski2022-07-19 07:40:552022-07-19 07:41:50New Report: Massachusetts Maintains Reasonable Debt Relative to GSP https://pioneerinstitute.org/wp-content/uploads/Picture1-2.png

247

624

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-06-09 10:58:442022-06-09 10:59:08As States Compete for Talent and Families, Massachusetts Experienced a Six-Fold Increase in Lost Wealth Compared to a Decade Earlier

https://pioneerinstitute.org/wp-content/uploads/Picture1-2.png

247

624

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-06-09 10:58:442022-06-09 10:59:08As States Compete for Talent and Families, Massachusetts Experienced a Six-Fold Increase in Lost Wealth Compared to a Decade Earlier https://pioneerinstitute.org/wp-content/uploads/Blog2Cover.png

382

763

Joseph Staruski

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Joseph Staruski2022-05-22 11:52:052022-06-03 16:54:15Massachusetts Tax Revenues Surpass Pre-Pandemic Levels

https://pioneerinstitute.org/wp-content/uploads/Blog2Cover.png

382

763

Joseph Staruski

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Joseph Staruski2022-05-22 11:52:052022-06-03 16:54:15Massachusetts Tax Revenues Surpass Pre-Pandemic Levels https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-17 05:55:222021-11-17 05:55:22Study: “Millionaire’s Tax” Would Have Far-Reaching Effects on “Pass-Through” Businesses

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-11-17 05:48:072021-11-17 05:48:07The Far-Reaching Impact of a Massachusetts Surtax: Anecdotal Evidence and Data Analysis

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-17 05:55:222021-11-17 05:55:22Study: “Millionaire’s Tax” Would Have Far-Reaching Effects on “Pass-Through” Businesses

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-11-17 05:48:072021-11-17 05:48:07The Far-Reaching Impact of a Massachusetts Surtax: Anecdotal Evidence and Data Analysis https://pioneerinstitute.org/wp-content/uploads/Hubwonk-Template-49.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-10-19 11:08:022021-10-19 11:19:34Competition Amongst States: How Tax Policy Drives Residents to Seek Better Value

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-Template-49.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-10-19 11:08:022021-10-19 11:19:34Competition Amongst States: How Tax Policy Drives Residents to Seek Better Value https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-10-07 06:10:092021-10-07 06:10:09A Timely Tax Cut: How New Hampshire is Taking Advantage of Massachusetts’ Graduated Income Tax Proposal

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-10-07 06:00:242021-10-07 06:00:24Study Warns that New Hampshire Tax Policies Would Exacerbate Impacts of a Graduated Income Tax

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-10-07 06:10:092021-10-07 06:10:09A Timely Tax Cut: How New Hampshire is Taking Advantage of Massachusetts’ Graduated Income Tax Proposal

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-10-07 06:00:242021-10-07 06:00:24Study Warns that New Hampshire Tax Policies Would Exacerbate Impacts of a Graduated Income Tax https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-11-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-09-27 05:54:502021-09-27 05:54:50Study Finds SALT Deduction Cap, Graduated Income Tax Will Combine to More Than Double Tax Burden on Some Households

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-11-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-09-27 05:54:502021-09-27 05:54:50Study Finds SALT Deduction Cap, Graduated Income Tax Will Combine to More Than Double Tax Burden on Some Households https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-1-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-08-10 05:39:222021-08-10 05:39:22Study Suggests How to Advance Fairness, Predictability of “Payment in Lieu of Taxes” Programs Aimed at Nonprofits

https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-1-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-08-10 05:39:222021-08-10 05:39:22Study Suggests How to Advance Fairness, Predictability of “Payment in Lieu of Taxes” Programs Aimed at Nonprofits https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-23.png

512

1024

Pioneer Institute

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Pioneer Institute2021-08-05 07:52:132021-08-05 07:54:42Public Statement on Implementation of the Charitable Giving Deduction

https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-23.png

512

1024

Pioneer Institute

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Pioneer Institute2021-08-05 07:52:132021-08-05 07:54:42Public Statement on Implementation of the Charitable Giving Deduction https://pioneerinstitute.org/wp-content/uploads/Tax-Flight-Photo-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-17 05:26:022021-06-17 09:24:04Study Says Massachusetts Surtax Proposal Could Reduce Taxable Income in the State by Over $2 Billion

https://pioneerinstitute.org/wp-content/uploads/Tax-Flight-Photo-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-17 05:26:022021-06-17 09:24:04Study Says Massachusetts Surtax Proposal Could Reduce Taxable Income in the State by Over $2 Billion https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-09 09:29:102021-06-09 09:29:10This Is No Time for a Tax Increase

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-09 09:29:102021-06-09 09:29:10This Is No Time for a Tax Increase https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-01 05:54:112021-06-01 05:54:11Study Finds Deep Flaws in Advocates’ Claims that the Massachusetts Tax Code is Regressive

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-01 05:54:112021-06-01 05:54:11Study Finds Deep Flaws in Advocates’ Claims that the Massachusetts Tax Code is Regressive https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-05-05 05:33:362021-05-05 06:04:38Study Says Interstate Tax Competition, Relocation Subsidies Exacerbate Telecommuting Trends

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-05-05 05:33:362021-05-05 06:04:38Study Says Interstate Tax Competition, Relocation Subsidies Exacerbate Telecommuting Trends https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-5.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-28 14:59:382021-11-23 10:55:03Statement before the MA Joint Committee on Revenue in Opposition to HB 86 (Pages 1-4) A legislative amendment to the Constitution to provide resources for education and transportation through an additional tax on incomes in excess of one million dollars.

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-5.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-28 14:59:382021-11-23 10:55:03Statement before the MA Joint Committee on Revenue in Opposition to HB 86 (Pages 1-4) A legislative amendment to the Constitution to provide resources for education and transportation through an additional tax on incomes in excess of one million dollars. https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-26 05:08:592021-04-26 05:22:50Study Warns Massachusetts Tax Proposal Would Deter Investment, Stifling the “Innovation Economy”

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-26 05:08:592021-04-26 05:22:50Study Warns Massachusetts Tax Proposal Would Deter Investment, Stifling the “Innovation Economy” https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Nina Weiss2021-04-20 05:38:152021-11-23 10:25:38The Graduated Income Tax Trap: A Tax on Small Businesses

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Nina Weiss2021-04-20 05:38:152021-11-23 10:25:38The Graduated Income Tax Trap: A Tax on Small Businesses https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-07 05:47:152021-04-07 05:47:15Study: Graduated Income Tax Proposal Fails to Protect Taxpayers from Bracket Creep

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-07 05:47:152021-04-07 05:47:15Study: Graduated Income Tax Proposal Fails to Protect Taxpayers from Bracket Creep https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-03-25 05:34:372021-12-29 12:19:26Missing the Mark on Wealth Migration: Past Studies Drastically Undercounted Millionaires

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-03-25 05:34:372021-12-29 12:19:26Missing the Mark on Wealth Migration: Past Studies Drastically Undercounted Millionaires https://pioneerinstitute.org/wp-content/uploads/Yellow-and-Green-2-Circle-Venn-Diagram-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-10 05:41:292021-03-10 06:28:08Study Finds Massachusetts Graduated Income Tax May Be a “Blank Check” and Not Increase Funding for Designated Priorities

https://pioneerinstitute.org/wp-content/uploads/Yellow-and-Green-2-Circle-Venn-Diagram-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-10 05:41:292021-03-10 06:28:08Study Finds Massachusetts Graduated Income Tax May Be a “Blank Check” and Not Increase Funding for Designated Priorities https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-1-2.png

512

1024

Jim Stergios

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Jim Stergios2021-03-03 09:12:142021-12-29 12:16:42Enacting ‘Millionaires’ Taxes’ Will Set Back State Recoveries

https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-1-2.png

512

1024

Jim Stergios

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Jim Stergios2021-03-03 09:12:142021-12-29 12:16:42Enacting ‘Millionaires’ Taxes’ Will Set Back State Recoveries https://pioneerinstitute.org/wp-content/uploads/Fig1-5.png

601

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

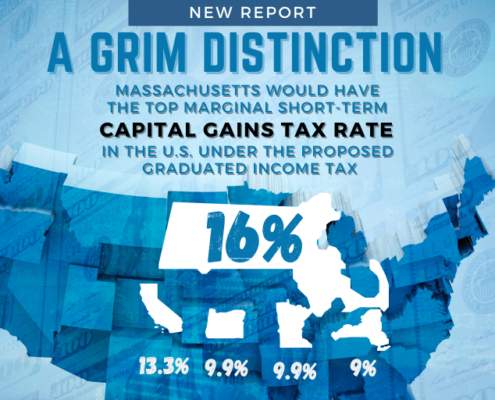

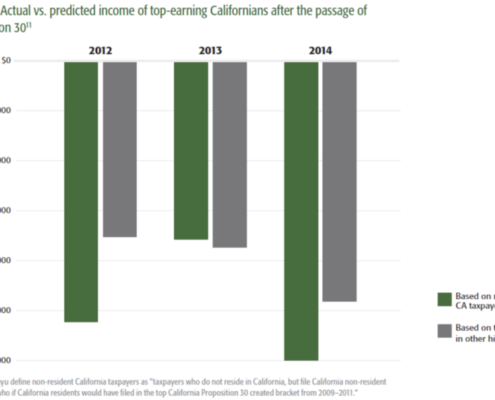

Editorial Staff2021-02-22 05:18:182021-02-22 06:08:55New Study Highlights Economic Fallout from California’s 2012 Tax Hike

https://pioneerinstitute.org/wp-content/uploads/Fig1-5.png

601

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-02-22 05:18:182021-02-22 06:08:55New Study Highlights Economic Fallout from California’s 2012 Tax Hike