https://pioneerinstitute.org/wp-content/uploads/Pioneer-Institute-Statement-on-Question-1.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-11-09 16:09:302022-11-09 16:09:30Pioneer Institute Statement on Question 1

https://pioneerinstitute.org/wp-content/uploads/Pioneer-Institute-Statement-on-Question-1.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-11-09 16:09:302022-11-09 16:09:30Pioneer Institute Statement on Question 1 https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-29 11:28:502022-07-29 11:28:50Pioneer Institute Expects That Massachusetts Taxpayers Will Be Refunded $3.2B Due To State Revenue Cap

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-29 11:28:502022-07-29 11:28:50Pioneer Institute Expects That Massachusetts Taxpayers Will Be Refunded $3.2B Due To State Revenue Cap https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-2-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-06 07:49:072022-07-06 07:54:29Survey of Business Sentiment: MA Income Tax Hike Would Lead to Employer Exodus

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-2-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-06 07:49:072022-07-06 07:54:29Survey of Business Sentiment: MA Income Tax Hike Would Lead to Employer Exodus https://pioneerinstitute.org/wp-content/uploads/Picture1-2.png

247

624

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

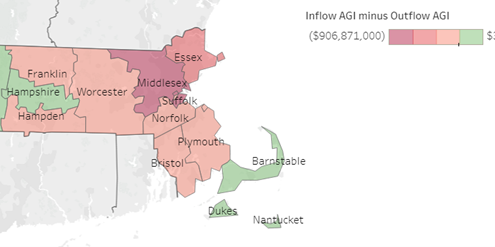

Editorial Staff2022-06-09 10:58:442022-06-09 10:59:08As States Compete for Talent and Families, Massachusetts Experienced a Six-Fold Increase in Lost Wealth Compared to a Decade Earlier

https://pioneerinstitute.org/wp-content/uploads/Picture1-2.png

247

624

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-06-09 10:58:442022-06-09 10:59:08As States Compete for Talent and Families, Massachusetts Experienced a Six-Fold Increase in Lost Wealth Compared to a Decade Earlier https://pioneerinstitute.org/wp-content/uploads/Untitled-design-2022-05-25T083008.246.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-05-25 08:30:492022-07-06 07:51:30Book Reveals How Tax Hike Amendment Would Damage Commonwealth’s Economic Competitiveness

https://pioneerinstitute.org/wp-content/uploads/Untitled-design-2022-05-25T083008.246.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-05-25 08:30:492022-07-06 07:51:30Book Reveals How Tax Hike Amendment Would Damage Commonwealth’s Economic Competitiveness https://pioneerinstitute.org/wp-content/uploads/public-statement-1.png

900

1600

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-27 11:57:102022-01-28 11:24:17Pioneer Supports Legal Challenge to Misleading Tax Ballot Language, Releases Video

https://pioneerinstitute.org/wp-content/uploads/public-statement-1.png

900

1600

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-27 11:57:102022-01-28 11:24:17Pioneer Supports Legal Challenge to Misleading Tax Ballot Language, Releases Video https://pioneerinstitute.org/wp-content/uploads/Understatement-web-post.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-18 06:52:502022-01-18 06:58:42Study: Tax Up For A Vote In November Would Ensnare Over Three Times More Taxpayers Than Previously Estimated

https://pioneerinstitute.org/wp-content/uploads/Understatement-web-post.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-18 06:52:502022-01-18 06:58:42Study: Tax Up For A Vote In November Would Ensnare Over Three Times More Taxpayers Than Previously Estimated https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-19 10:49:272021-11-19 10:49:27Public Statement on Massachusetts High Technology Council’s Challenge to the Graduated Income Tax Ballot Language

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-19 10:49:272021-11-19 10:49:27Public Statement on Massachusetts High Technology Council’s Challenge to the Graduated Income Tax Ballot Language https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-17 05:55:222021-11-17 05:55:22Study: “Millionaire’s Tax” Would Have Far-Reaching Effects on “Pass-Through” Businesses

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-11-17 05:55:222021-11-17 05:55:22Study: “Millionaire’s Tax” Would Have Far-Reaching Effects on “Pass-Through” Businesses https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-10-07 06:00:242021-10-07 06:00:24Study Warns that New Hampshire Tax Policies Would Exacerbate Impacts of a Graduated Income Tax

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-10-07 06:00:242021-10-07 06:00:24Study Warns that New Hampshire Tax Policies Would Exacerbate Impacts of a Graduated Income Tax https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-11-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-09-27 05:54:502021-09-27 05:54:50Study Finds SALT Deduction Cap, Graduated Income Tax Will Combine to More Than Double Tax Burden on Some Households

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-11-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-09-27 05:54:502021-09-27 05:54:50Study Finds SALT Deduction Cap, Graduated Income Tax Will Combine to More Than Double Tax Burden on Some Households https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-09 09:29:102021-06-09 09:29:10This Is No Time for a Tax Increase

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-09 09:29:102021-06-09 09:29:10This Is No Time for a Tax Increase https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-01 05:54:112021-06-01 05:54:11Study Finds Deep Flaws in Advocates’ Claims that the Massachusetts Tax Code is Regressive

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-01 05:54:112021-06-01 05:54:11Study Finds Deep Flaws in Advocates’ Claims that the Massachusetts Tax Code is Regressive https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-05-05 05:33:362021-05-05 06:04:38Study Says Interstate Tax Competition, Relocation Subsidies Exacerbate Telecommuting Trends

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-05-05 05:33:362021-05-05 06:04:38Study Says Interstate Tax Competition, Relocation Subsidies Exacerbate Telecommuting Trends https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-26 05:08:592021-04-26 05:22:50Study Warns Massachusetts Tax Proposal Would Deter Investment, Stifling the “Innovation Economy”

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-26 05:08:592021-04-26 05:22:50Study Warns Massachusetts Tax Proposal Would Deter Investment, Stifling the “Innovation Economy” https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-20 05:46:542021-04-20 15:51:32Study Shows the Adverse Effects of Graduated Income Tax Proposal on Small Businesses

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-20 05:46:542021-04-20 15:51:32Study Shows the Adverse Effects of Graduated Income Tax Proposal on Small Businesses https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-07 05:47:152021-04-07 05:47:15Study: Graduated Income Tax Proposal Fails to Protect Taxpayers from Bracket Creep

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-07 05:47:152021-04-07 05:47:15Study: Graduated Income Tax Proposal Fails to Protect Taxpayers from Bracket Creep https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-01 05:56:422021-04-01 07:11:11New Study Warns Graduated Income Tax Will Harm Many Massachusetts Retirees

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-01 05:56:422021-04-01 07:11:11New Study Warns Graduated Income Tax Will Harm Many Massachusetts Retirees https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-25 05:46:072021-04-01 06:00:36Study: Graduated Income Tax Proponents Rely on Analyses That Exclude the Vast Majority Of “Millionaires” to Argue Their Case

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-25 05:46:072021-04-01 06:00:36Study: Graduated Income Tax Proponents Rely on Analyses That Exclude the Vast Majority Of “Millionaires” to Argue Their Case https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

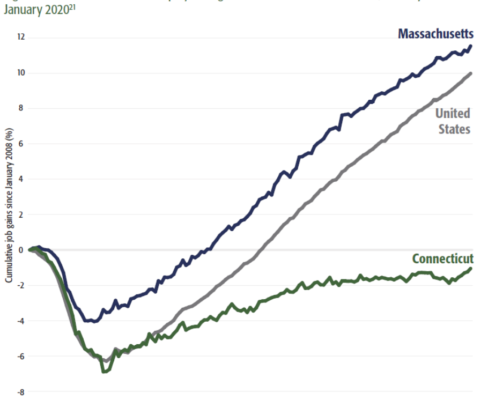

Editorial Staff2021-03-15 05:43:412021-03-15 05:45:37Report Contrasts State Government and Private Sector Employment Changes During Pandemic

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-15 05:43:412021-03-15 05:45:37Report Contrasts State Government and Private Sector Employment Changes During Pandemic https://pioneerinstitute.org/wp-content/uploads/Yellow-and-Green-2-Circle-Venn-Diagram-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-10 05:41:292021-03-10 06:28:08Study Finds Massachusetts Graduated Income Tax May Be a “Blank Check” and Not Increase Funding for Designated Priorities

https://pioneerinstitute.org/wp-content/uploads/Yellow-and-Green-2-Circle-Venn-Diagram-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-10 05:41:292021-03-10 06:28:08Study Finds Massachusetts Graduated Income Tax May Be a “Blank Check” and Not Increase Funding for Designated Priorities https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-02 05:55:462021-03-02 06:36:19Report: Proposed Graduated Income Tax Might Not Increase State Education and Transportation Spending

https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-02 05:55:462021-03-02 06:36:19Report: Proposed Graduated Income Tax Might Not Increase State Education and Transportation Spending https://pioneerinstitute.org/wp-content/uploads/Fig1-5.png

601

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

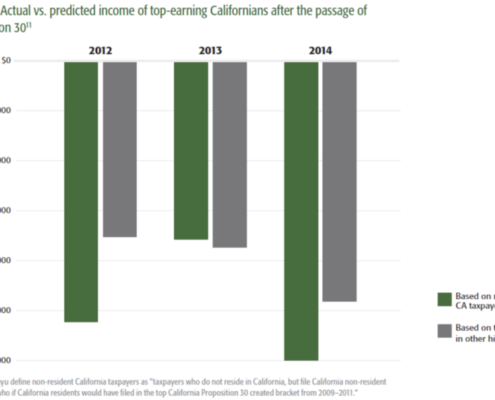

Editorial Staff2021-02-22 05:18:182021-02-22 06:08:55New Study Highlights Economic Fallout from California’s 2012 Tax Hike

https://pioneerinstitute.org/wp-content/uploads/Fig1-5.png

601

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-02-22 05:18:182021-02-22 06:08:55New Study Highlights Economic Fallout from California’s 2012 Tax Hike https://pioneerinstitute.org/wp-content/uploads/Fig1-4.png

831

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

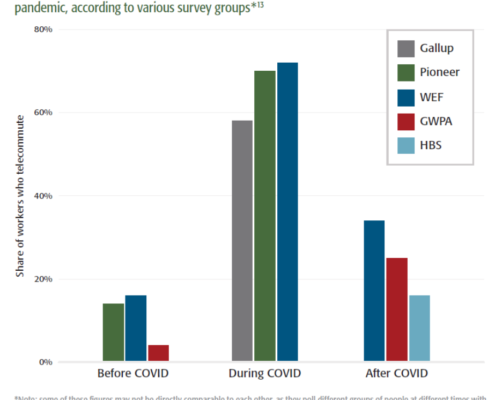

Editorial Staff2021-02-10 05:29:552021-03-22 13:57:11New Study Finds Pandemic-Spurred Technologies Lowered Barriers to Exit in High-Cost States

https://pioneerinstitute.org/wp-content/uploads/Fig1-4.png

831

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-02-10 05:29:552021-03-22 13:57:11New Study Finds Pandemic-Spurred Technologies Lowered Barriers to Exit in High-Cost States https://pioneerinstitute.org/wp-content/uploads/Fig1-3.png

652

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

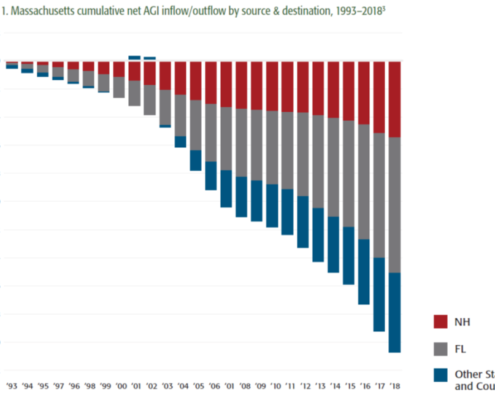

Editorial Staff2021-02-01 05:10:572021-07-22 09:09:56New Study Shows Significant Wealth Migration from Massachusetts to Florida, New Hampshire

https://pioneerinstitute.org/wp-content/uploads/Fig1-3.png

652

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-02-01 05:10:572021-07-22 09:09:56New Study Shows Significant Wealth Migration from Massachusetts to Florida, New Hampshire https://pioneerinstitute.org/wp-content/uploads/JoshRauh.jpg

390

278

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-01-19 10:47:172021-03-22 13:59:45California Tax Experiment: Policy Makers Receive Valuable Economics Lesson

https://pioneerinstitute.org/wp-content/uploads/JoshRauh.jpg

390

278

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-01-19 10:47:172021-03-22 13:59:45California Tax Experiment: Policy Makers Receive Valuable Economics Lesson https://pioneerinstitute.org/wp-content/uploads/CT-Fig-3.png

806

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-01-14 05:48:432021-02-15 16:11:15New Study Finds Tax Policy Drives Connecticut’s Ongoing Fiscal & Economic Crisis

https://pioneerinstitute.org/wp-content/uploads/CT-Fig-3.png

806

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-01-14 05:48:432021-02-15 16:11:15New Study Finds Tax Policy Drives Connecticut’s Ongoing Fiscal & Economic Crisis https://pioneerinstitute.org/wp-content/uploads/home-for-sale.jpg

480

720

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2018-05-21 08:00:412020-12-07 17:57:48Study: Methodology of Noted “Millionaire’s Tax” Researcher Excludes Vast Majority of Millionaires

https://pioneerinstitute.org/wp-content/uploads/home-for-sale.jpg

480

720

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2018-03-26 09:23:002020-12-07 17:58:25Inadequate Inflation Adjustment Factor Will Subject Increasing Numbers of People to So-Called “Millionaires” Tax

https://pioneerinstitute.org/wp-content/uploads/home-for-sale.jpg

480

720

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2018-05-21 08:00:412020-12-07 17:57:48Study: Methodology of Noted “Millionaire’s Tax” Researcher Excludes Vast Majority of Millionaires

https://pioneerinstitute.org/wp-content/uploads/home-for-sale.jpg

480

720

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2018-03-26 09:23:002020-12-07 17:58:25Inadequate Inflation Adjustment Factor Will Subject Increasing Numbers of People to So-Called “Millionaires” Tax