Study Finds Pension Obligation Bonds Could Worsen T Retirement Fund’s Financial Woes

BOSTON – A new study published by Pioneer Institute finds that issuing pension obligation bonds (POBs) to refinance $360 million of the MBTA Retirement Fund’s (MBTARF’s) $1.3 billion unfunded pension liability would only compound the T’s already serious financial risks.

With POBs, government entities deposit revenues from bond sales into their pension funds and use the money to make investments they hope will deliver returns that outpace borrowing costs.

“Virtually every study of POBs finds that timing and duration of the bond issues are critical,” said E.J. McMahon, author of “Rolling the Retirement Dice.” “Bonds floated at the end of a bull market are the most likely to lose money, and that makes this idea a wrong turn at the worst possible time.”

If investments don’t meet a pension fund’s assumed rate of return, it could be left with debt service costs in addition to the pre-existing unfunded liability. In 2015, the Government Finance Officers Association bluntly warned that “State and local governments should not issue POBs.” It reaffirmed its guidance last year.

If the MBTA were a private company, federal law would require it to base the expected rate of return on its pension investments on the current and historic yields for low-risk assets such as high-quality corporate bonds. These returns are currently around 4 percent.

But under more permissive government accounting standards, the MBTA has set its expected rate of return at 7.25 percent annually.

The MBTARF is currently projected to require $3.07 billion to cover pension expenses through the lifespans of its youngest vested employees, but its assets come up about $1.3 billion short. Assuming the more conservative 4 percent rate of return, total liability rises to over $4 billion.

As recently as 2007, the MBTARF had more than 90 percent of the assets needed to meet its obligations. Yet despite annual employer (MBTA) contributions that rose from $21 million in 2001 to $148 million last year, the retirement fund was only 53.55 percent funded by fiscal 2020. Among large U.S. transit agencies, only Chicago has a lower funding ratio and a larger unfunded liability.

The T contributes 26.7 percent of covered salaries to the MBTARF, while employees kick in 9.33 percent of pre-tax salaries. Two thirds of the money goes toward the unfunded liability, not the “normal cost” of new pension liability that accrues each year.

McMahon identifies several issues behind these problems. The first is poor investment management. A 2016 Pioneer study found that the MBTARF would have earned an additional $900 million between 2001 and 2014 if it deposited its funds in the better performing Massachusetts State Employee Retirement System.

The second reason is that the T underfunded the MBTARF by $66 million from 2007 to 2014. If it had made its full contribution during those years, that $66 million would have grown to $183 million by the end of 2021.

Meanwhile, annual pension benefits continue to grow, from $96 million in 2001 to $220 million in 2020.

Finally, in large part because the majority of T employees can retire in their 40s or 50s, the MBTARF has fewer active employees paying into the fund than retired transit workers drawing pensions. The MBTARF has 0.845 active employees for each person collecting pension benefits. Overall, the state average for active employees-to-beneficiaries is 1.358. The MBTARF is one of only four of 105 public pension funds in Massachusetts that has more beneficiaries than contributors.

Underlying all these issues are the MBTA’s fundamental budgetary challenges. Fare revenue is projected to remain 25 percent below pre-pandemic levels through fiscal 2023, and the Authority will have to draw down reserves to balance its $2.6 billion budget.

“The T’s financial condition requires fiscal prudence, not a risky quick fix like pension obligation bonds,” said Pioneer Executive Director Jim Stergios. “Such ploys rarely work – and a bit like a Hail Mary pass, it’s the wrong play to call especially right now.”

About the Author

E.J. McMahon is a public policy analyst focused on state and regional economic, fiscal, and demographic trends. McMahon is founding senior fellow of the Empire Center for Public Policy in Albany, New York, and an adjunct fellow at the Manhattan Institute for Policy Research. A former journalist, he also served in senior staff positions in New York state government. McMahon is a graduate of Villanova University.

Pioneer Institute develops and communicates dynamic ideas that advance prosperity and a vibrant civic life in Massachusetts and beyond. Success for Pioneer is when the citizens of our state and nation prosper and our society thrives because we enjoy world-class options in education, healthcare, transportation and economic opportunity, and when our government is limited, accountable and transparent. Pioneer believes that America is at its best when our citizenry is well-educated, committed to liberty, personal responsibility, and free enterprise, and both willing and able to test their beliefs based on facts and the free exchange of ideas.

Get Updates on Our Transportation Research

Related Posts:

https://pioneerinstitute.org/wp-content/uploads/amtrak.png

532

845

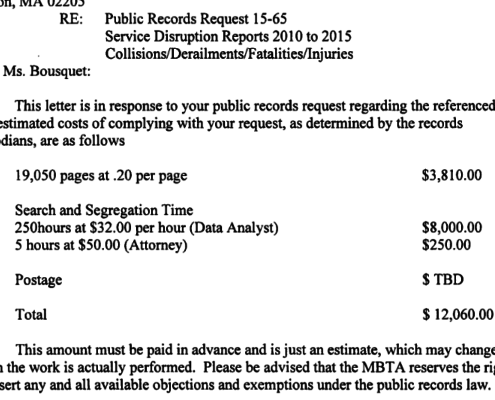

MuckRock

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

MuckRock2015-05-13 11:47:172019-07-11 11:31:04The High Cost of Records Requests at the MBTA Hits a New Low

https://pioneerinstitute.org/wp-content/uploads/amtrak.png

532

845

MuckRock

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

MuckRock2015-05-13 11:47:172019-07-11 11:31:04The High Cost of Records Requests at the MBTA Hits a New Low https://pioneerinstitute.org/wp-content/uploads/RedLineCharlesMGH1.jpg

768

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2015-05-11 12:35:002019-07-11 11:31:04Testimony: Why Pioneer Supports MBTA Reform

https://pioneerinstitute.org/wp-content/uploads/RedLineCharlesMGH1.jpg

768

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2015-05-11 12:35:002019-07-11 11:31:04Testimony: Why Pioneer Supports MBTA Reform https://pioneerinstitute.org/wp-content/uploads/house-of-cards.jpg

183

275

Jim Stergios

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Jim Stergios2015-05-02 10:49:592015-05-04 06:26:44The Convention Center Expansion was a House of Cards

https://pioneerinstitute.org/wp-content/uploads/house-of-cards.jpg

183

275

Jim Stergios

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Jim Stergios2015-05-02 10:49:592015-05-04 06:26:44The Convention Center Expansion was a House of Cards https://pioneerinstitute.org/wp-content/uploads/MBTA-Keolis-Performance-Feature.jpg

623

930

Scott Haller

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Scott Haller2015-04-15 15:10:392019-07-11 11:31:04Is Keolis Up to the Task?

https://pioneerinstitute.org/wp-content/uploads/MBTA-Keolis-Performance-Feature.jpg

623

930

Scott Haller

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Scott Haller2015-04-15 15:10:392019-07-11 11:31:04Is Keolis Up to the Task? https://pioneerinstitute.org/wp-content/uploads/RIDE.jpg

307

410

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2015-04-07 15:59:292019-07-11 11:31:04What if “The Ride” operated like the best big paratransit systems in the US?

https://pioneerinstitute.org/wp-content/uploads/RIDE.jpg

307

410

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2015-04-07 15:59:292019-07-11 11:31:04What if “The Ride” operated like the best big paratransit systems in the US? https://pioneerinstitute.org/wp-content/uploads/THERIDEbus.jpg

243

500

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2015-04-07 10:37:222019-07-11 11:31:04Guess Who Runs the Best Paratransit System in the MBTA’s District? Hint: It’s Not the T

https://pioneerinstitute.org/wp-content/uploads/THERIDEbus.jpg

243

500

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2015-04-07 10:37:222019-07-11 11:31:04Guess Who Runs the Best Paratransit System in the MBTA’s District? Hint: It’s Not the T https://pioneerinstitute.org/wp-content/uploads/Top-Secret11.jpg

334

623

Mary Connaughton

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Mary Connaughton2015-04-07 10:03:442015-04-07 10:03:44Public Left in Dark on Carmen’s Union Contract

https://pioneerinstitute.org/wp-content/uploads/Top-Secret11.jpg

334

623

Mary Connaughton

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

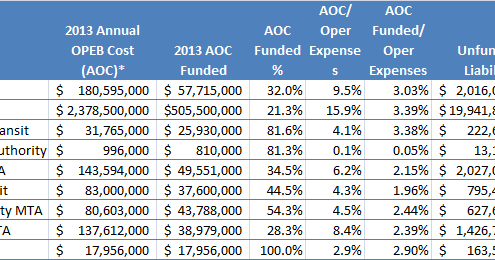

Mary Connaughton2015-04-07 10:03:442015-04-07 10:03:44Public Left in Dark on Carmen’s Union Contract https://pioneerinstitute.org/wp-content/uploads/OPEB.png

260

718

Mary Connaughton

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Mary Connaughton2015-04-06 12:03:362019-07-11 11:32:26And What About the T’s Retirement Costs?

https://pioneerinstitute.org/wp-content/uploads/OPEB.png

260

718

Mary Connaughton

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Mary Connaughton2015-04-06 12:03:362019-07-11 11:32:26And What About the T’s Retirement Costs? https://pioneerinstitute.org/wp-content/uploads/MBTAvSEPTA-640x341.jpg

399

726

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2015-04-02 12:03:422021-01-28 15:23:53The MBTA Commuter Rail’s Cost Structure Is Off the Rails

https://pioneerinstitute.org/wp-content/uploads/MBTAvSEPTA-640x341.jpg

399

726

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2015-04-02 12:03:422021-01-28 15:23:53The MBTA Commuter Rail’s Cost Structure Is Off the Rails https://pioneerinstitute.org/wp-content/uploads/MBTA-Winter-Recap-Feature.jpg

854

1280

Scott Haller

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Scott Haller2015-03-30 15:32:592019-07-11 11:32:26Sunshine Must Return to MBTA This Spring

https://pioneerinstitute.org/wp-content/uploads/MBTA-Winter-Recap-Feature.jpg

854

1280

Scott Haller

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Scott Haller2015-03-30 15:32:592019-07-11 11:32:26Sunshine Must Return to MBTA This Spring