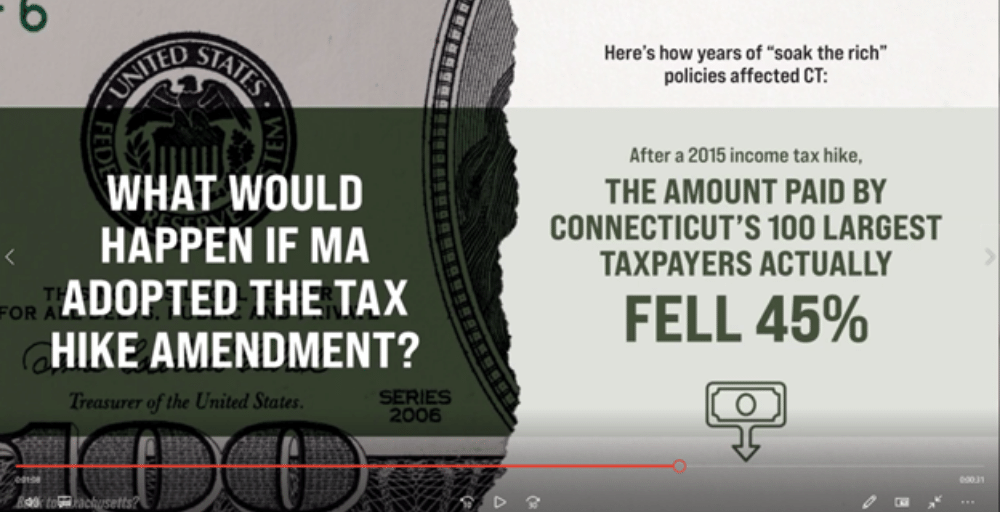

How did tax hikes work out for Connecticut?

Watch: In our newest video, Pioneer Institute’s Charlie Chieppo shares data on the economic impact of tax increases in Connecticut – which has the 2nd highest state and local tax burden in the country and ranks 49th in private sector wage and job growth. As Massachusetts considers a proposal to raise income taxes, it is important to learn from the experience of other states. Learn more.

Get Updates on Our Economic Opportunity Research

Additional Pioneer reports on the Mass. economy:

Related Posts

https://pioneerinstitute.org/wp-content/uploads/Op-ed-Schedule-A-Enright-01292024.png

1400

1400

Aidan Enright

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Aidan Enright2024-01-29 15:39:002024-08-01 07:01:40Skill-based immigration could ease labor shortage

https://pioneerinstitute.org/wp-content/uploads/Op-ed-Schedule-A-Enright-01292024.png

1400

1400

Aidan Enright

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Aidan Enright2024-01-29 15:39:002024-08-01 07:01:40Skill-based immigration could ease labor shortage https://pioneerinstitute.org/wp-content/uploads/Screenshot-2023-10-30-at-3.45.55-PM.png

1334

1570

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

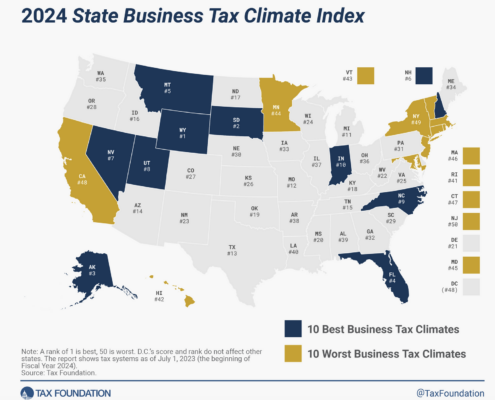

Editorial Staff2023-10-30 15:47:462023-10-30 15:47:46Statement on Massachusetts Falling from 34th to 46th on Tax Foundation’s 2024 Business Tax Climate Index

https://pioneerinstitute.org/wp-content/uploads/Screenshot-2023-10-30-at-3.45.55-PM.png

1334

1570

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-10-30 15:47:462023-10-30 15:47:46Statement on Massachusetts Falling from 34th to 46th on Tax Foundation’s 2024 Business Tax Climate Index https://pioneerinstitute.org/wp-content/uploads/Chapter-62F-09292023.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-09-28 16:14:372023-09-28 16:31:13Poll: MA Voters Oppose Legislative Proposals to Change Tax Rebate Law

https://pioneerinstitute.org/wp-content/uploads/Chapter-62F-09292023.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-09-28 16:14:372023-09-28 16:31:13Poll: MA Voters Oppose Legislative Proposals to Change Tax Rebate Law https://pioneerinstitute.org/wp-content/uploads/Bike-lanes-op-ed-image.png

1400

1400

Barbara Anthony

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Barbara Anthony2023-06-12 11:19:362023-07-10 10:40:12Installing bike and bus lanes requires public debate

https://pioneerinstitute.org/wp-content/uploads/Bike-lanes-op-ed-image.png

1400

1400

Barbara Anthony

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Barbara Anthony2023-06-12 11:19:362023-07-10 10:40:12Installing bike and bus lanes requires public debate https://pioneerinstitute.org/wp-content/uploads/Immigrant-Entre-image.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-06-08 09:01:272024-08-01 07:36:17Study: Immigrant Entrepreneurs Benefit N.E. Economy, Despite Facing Obstacles to Growth

https://pioneerinstitute.org/wp-content/uploads/Immigrant-Entre-image.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-06-08 09:01:272024-08-01 07:36:17Study: Immigrant Entrepreneurs Benefit N.E. Economy, Despite Facing Obstacles to Growth https://pioneerinstitute.org/wp-content/uploads/Statement-on-tax-reform-and-budget.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-19 09:00:272023-04-19 09:27:17Public Statement on the House’s Proposed Tax Reform and Budget

https://pioneerinstitute.org/wp-content/uploads/Statement-on-tax-reform-and-budget.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-19 09:00:272023-04-19 09:27:17Public Statement on the House’s Proposed Tax Reform and Budget https://pioneerinstitute.org/wp-content/uploads/Nail-salons-image.webp

574

907

Charles Chieppo

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Charles Chieppo2023-02-22 15:11:052024-08-01 06:51:10Licensing burdens thwart economic growth in Massachusetts

https://pioneerinstitute.org/wp-content/uploads/Nail-salons-image.webp

574

907

Charles Chieppo

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Charles Chieppo2023-02-22 15:11:052024-08-01 06:51:10Licensing burdens thwart economic growth in Massachusetts https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-13.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-12-08 08:13:462024-08-01 07:50:42Report: Immigrant Entrepreneurs Provide Economic Benefits, but Face Significant Obstacles

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-13.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-12-08 08:13:462024-08-01 07:50:42Report: Immigrant Entrepreneurs Provide Economic Benefits, but Face Significant Obstacles https://pioneerinstitute.org/wp-content/uploads/Pioneer-Institute-Statement-on-Question-1.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-11-09 16:09:302022-11-09 16:09:30Pioneer Institute Statement on Question 1

https://pioneerinstitute.org/wp-content/uploads/Pioneer-Institute-Statement-on-Question-1.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-11-09 16:09:302022-11-09 16:09:30Pioneer Institute Statement on Question 1 https://pioneerinstitute.org/wp-content/uploads/MassachusettsStateHouse-1.jpg

2592

3872

Charles Chieppo

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Charles Chieppo2022-11-07 14:11:352022-11-07 14:11:35Taxachusetts Must Be Stopped

https://pioneerinstitute.org/wp-content/uploads/MassachusettsStateHouse-1.jpg

2592

3872

Charles Chieppo

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Charles Chieppo2022-11-07 14:11:352022-11-07 14:11:35Taxachusetts Must Be Stopped https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-09-21 10:16:452022-09-21 12:05:41Study: Legislators Must Answer Key Questions Before Setting Policy for App-Based Rideshare/Delivery Workers

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-09-21 10:16:452022-09-21 12:05:41Study: Legislators Must Answer Key Questions Before Setting Policy for App-Based Rideshare/Delivery Workers https://pioneerinstitute.org/wp-content/uploads/WSJ-web.png

512

1024

Jim Stergios

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Jim Stergios2022-09-09 17:20:182022-09-09 17:20:18WSJ op-ed: Don’t Make Massachusetts ‘Taxachusetts’ Again

https://pioneerinstitute.org/wp-content/uploads/WSJ-web.png

512

1024

Jim Stergios

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Jim Stergios2022-09-09 17:20:182022-09-09 17:20:18WSJ op-ed: Don’t Make Massachusetts ‘Taxachusetts’ Again