Report: Proposed Graduated Income Tax Might Not Increase State Education and Transportation Spending

Legislature could devote new revenue to public education and transportation, but cut funding from existing sources by the same amount

BOSTON – While supporters of a Massachusetts constitutional amendment that would impose a 4 percent tax rate hike on annual income over $1 million claim additional revenue from the surtax will fund public education and transportation needs, the amendment in no way assures that there will be new spending on these priorities. In fact, without violating the amendment, total state education and transportation funding could stay the same or even fall, according to a new review published by Pioneer Institute.

Total state education and transportation funding is currently around $8.5 billion annually. Under the proposed amendment, the Legislature could dedicate the nearly $2 billion in additional revenue supporters of the graduated income tax claim it would generate to education and transportation, but cut funding from other sources from $8.5 billion to $6.5 billion, leaving total state spending in those areas exactly where it had been before.

“As a practical matter, every dollar the graduated income tax generates could be siphoned off to some other purpose without violating the text of the proposed constitutional amendment,” said Kevin Martin, author of “The Graduated Income Tax Amendment – A Shell Game?”

The Massachusetts Constitution requires a flat income tax rate. On five occasions in the last 60 years, voters were asked to amend the constitution to eliminate the ban on a graduated tax rate. Each time they refused.

In the runup to the 2018 election cycle, proponents of a graduated income tax attempted to overcome the unpopularity of their cause by earmarking new revenue from a 4 percent rate hike on annual income over $1 million for public education and transportation spending.

The proposed constitutional amendment never made it to the voters. The Commonwealth’s Supreme Judicial Court (SJC) ruled in Anderson v. Healey that the proposed amendment violated a ban on citizen-initiated ballot questions that combine unrelated subjects, as the amendment proposed both a new graduated income tax and a directive that any additional revenues would go to two disparate spending areas.

The court’s assertion of a constitutional ban on combining unrelated subjects does not apply to constitutional amendments proposed by the Legislature. In 2019, Beacon Hill tax hike supporters responded to the court’s decision by voting to approve the graduated income tax in a constitutional convention vote. If passed at a second constitutional convention, the measure will be placed as a question on the 2022 statewide ballot.

Attorney General Maura Healey’s own brief in the 2018 case reads: “the Legislature could choose to reduce spending in specified budget categories from other sources and replace it with new surtax revenue.”

When the late SJC Chief Justice Ralph Gants asked the Attorney General’s counsel during oral argument whether she agreed that, if the graduated income tax passed, it “may or may not result in any increase in education or transportation spending,” counsel responded that the Chief Justice’s understanding was correct.

More recently, during legislative debates on the proposed ballot measure, an amendment was offered that would have required the new tax revenues to be spent incrementally on education and transportation, over and above what already is spent. That amendment was defeated.

“Massachusetts’ flat income tax rate of 5 percent has served the state well. The Bay State has outcompeted our regional rivals and drawn in jobs and investment from higher-tax jurisdictions like New York, Connecticut, and California,” said Pioneer Executive Director Jim Stergios. “The debate on the graduated tax is simply this: does the Legislature care more about attracting jobs and investment to the private sector, which represents 97 percent of Massachusetts workers, or will they bow to the wishes of powerful public sector unions who represent 3 percent of Massachusetts workers? The question is especially important now given how hard-hit private sector employment was by the pandemic.”

About the Author

Kevin Martin is a partner and co-chair of the Appellate Litigation Group at Goodwin Procter LLP in Boston, where he has practiced since 2001. He was counsel for the plaintiffs in Anderson v. Healey, the 2018 decision in which the Supreme Judicial Court excluded the graduated income tax from that year’s ballot. Prior to joining Goodwin, Kevin clerked for U.S. Supreme Court Justice Antonin Scalia (2000-2001), and Judge Laurence Silberman on the U.S. Court of Appeals for the District of Columbia Circuit (1999-2000). From 2010-2011, he served as deputy independent counsel representing the SJC in an investigation into corruption in the Massachusetts Probation Department. He currently is vice chair of the board of directors of the New England Legal Foundation. Kevin graduated from Columbia Law School in 1999 and Georgetown University’s School of Foreign Service in 1996.

About Pioneer

Pioneer’s mission is to develop and communicate dynamic ideas that advance prosperity and a vibrant civic life in Massachusetts and beyond.

Pioneer’s vision of success is a state and nation where our people can prosper and our society thrive because we enjoy world-class options in education, healthcare, transportation and economic opportunity, and where our government is limited, accountable and transparent.

Pioneer values an America where our citizenry is well-educated and willing to test our beliefs based on facts and the free exchange of ideas, and committed to liberty, personal responsibility, and free enterprise.

Get Updates on Our Economic Opportunity Research

Related Content

https://pioneerinstitute.org/wp-content/uploads/Economic-Revitalization-and-Reinvention-in-Lowell-1998-2018-5.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-11-23 07:43:362020-12-07 17:05:44Pioneer Report Spotlights Decade-long Building Boom in Massachusetts Construction Industry

https://pioneerinstitute.org/wp-content/uploads/Economic-Revitalization-and-Reinvention-in-Lowell-1998-2018-5.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-11-23 07:43:362020-12-07 17:05:44Pioneer Report Spotlights Decade-long Building Boom in Massachusetts Construction Industry https://pioneerinstitute.org/wp-content/uploads/Economic-Revitalization-and-Reinvention-in-Lowell-1998-2018-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-11-19 08:00:132020-11-19 08:48:28Pioneer Checklist Includes Steps for Policy Makers, Business Owners to Revitalize Hardest-Hit Industries

https://pioneerinstitute.org/wp-content/uploads/Economic-Revitalization-and-Reinvention-in-Lowell-1998-2018-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-11-19 08:00:132020-11-19 08:48:28Pioneer Checklist Includes Steps for Policy Makers, Business Owners to Revitalize Hardest-Hit Industries https://pioneerinstitute.org/wp-content/uploads/Economic-Revitalization-and-Reinvention-in-Lowell-1998-2018-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-11-16 07:35:202020-12-07 17:07:12Pioneer Report Highlights Pre-Pandemic Employment Growth in Massachusetts’ Hospitality & Food Industry

https://pioneerinstitute.org/wp-content/uploads/Economic-Revitalization-and-Reinvention-in-Lowell-1998-2018-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-11-16 07:35:202020-12-07 17:07:12Pioneer Report Highlights Pre-Pandemic Employment Growth in Massachusetts’ Hospitality & Food Industry https://pioneerinstitute.org/wp-content/uploads/Economic-Revitalization-and-Reinvention-in-Lowell-1998-2018.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-10-26 10:16:112020-12-07 17:08:28Pioneer Report Highlights Employment Growth in Lowell, Massachusetts

https://pioneerinstitute.org/wp-content/uploads/Economic-Revitalization-and-Reinvention-in-Lowell-1998-2018.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-10-26 10:16:112020-12-07 17:08:28Pioneer Report Highlights Employment Growth in Lowell, Massachusetts https://pioneerinstitute.org/wp-content/uploads/Schneier.jpg

265

265

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-10-13 10:16:132021-01-28 15:28:40Ballot Question 1: Risks & Regulations Regarding Right to Repair

https://pioneerinstitute.org/wp-content/uploads/Schneier.jpg

265

265

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-10-13 10:16:132021-01-28 15:28:40Ballot Question 1: Risks & Regulations Regarding Right to Repair https://pioneerinstitute.org/wp-content/uploads/mikula.jpg

200

200

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-10-06 09:57:222021-02-15 15:48:24Small Business Life Support: Policy Relief for Firms Sickened by COVID?

https://pioneerinstitute.org/wp-content/uploads/mikula.jpg

200

200

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-10-06 09:57:222021-02-15 15:48:24Small Business Life Support: Policy Relief for Firms Sickened by COVID? https://pioneerinstitute.org/wp-content/uploads/Broad-Industry-Sector-Trends-in-Massachusetts-1998-2018-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-09-28 10:17:402021-01-28 14:55:46Pioneer Report Underscores Wide Disparities in Economic Performance between Industry Sectors in Massachusetts

https://pioneerinstitute.org/wp-content/uploads/Broad-Industry-Sector-Trends-in-Massachusetts-1998-2018-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-09-28 10:17:402021-01-28 14:55:46Pioneer Report Underscores Wide Disparities in Economic Performance between Industry Sectors in Massachusetts https://pioneerinstitute.org/wp-content/uploads/Five-Reasons-Why-Drug-Rebates-Are-Harmful-to-Patients-and-to-the-Healthcare-System-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

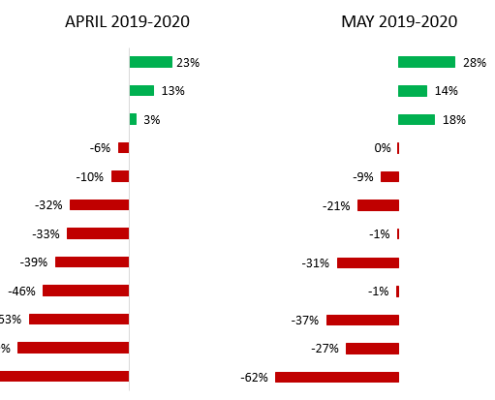

Editorial Staff2020-09-24 08:00:262020-12-11 13:11:37Study: Economic Recovery from COVID Will Require Short-Term Relief, Long-Term Reforms

https://pioneerinstitute.org/wp-content/uploads/Five-Reasons-Why-Drug-Rebates-Are-Harmful-to-Patients-and-to-the-Healthcare-System-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-09-24 08:00:262020-12-11 13:11:37Study: Economic Recovery from COVID Will Require Short-Term Relief, Long-Term Reforms https://pioneerinstitute.org/wp-content/uploads/Dollar-bills-1.jpg

1079

1527

Thomas O'Rourke

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Thomas O'Rourke2020-08-14 10:00:422020-08-13 09:52:45Massachusetts PPP Benefits Big Businesses, Data Called Into Question

https://pioneerinstitute.org/wp-content/uploads/Dollar-bills-1.jpg

1079

1527

Thomas O'Rourke

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Thomas O'Rourke2020-08-14 10:00:422020-08-13 09:52:45Massachusetts PPP Benefits Big Businesses, Data Called Into Question https://pioneerinstitute.org/wp-content/uploads/PPP-blog-1.3.png

661

911

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

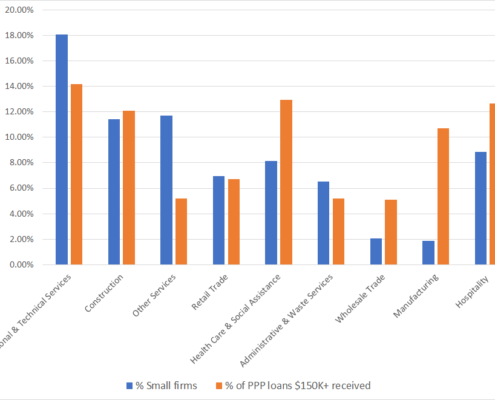

Nina Weiss2020-08-13 10:00:412021-01-28 15:24:57Where Did the Largest PPP Loans Go? Assessing the distribution of loans by industry

https://pioneerinstitute.org/wp-content/uploads/PPP-blog-1.3.png

661

911

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Nina Weiss2020-08-13 10:00:412021-01-28 15:24:57Where Did the Largest PPP Loans Go? Assessing the distribution of loans by industry https://pioneerinstitute.org/wp-content/uploads/The-Potry-of-Jazz-3.png

1440

2560

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-08-11 10:36:502021-01-28 14:50:37Non-Profits Facing COVID-19: Charles River’s Esplanade Association on Why It’s No Walk in the Park

https://pioneerinstitute.org/wp-content/uploads/The-Potry-of-Jazz-3.png

1440

2560

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2020-08-11 10:36:502021-01-28 14:50:37Non-Profits Facing COVID-19: Charles River’s Esplanade Association on Why It’s No Walk in the Park https://pioneerinstitute.org/wp-content/uploads/retail-sales-2.png

413

1054

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Nina Weiss2020-08-03 11:00:272021-01-28 15:11:39Data, Attitudes, and Ecommerce: Noteworthy trends in retail for the present and future

https://pioneerinstitute.org/wp-content/uploads/retail-sales-2.png

413

1054

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Nina Weiss2020-08-03 11:00:272021-01-28 15:11:39Data, Attitudes, and Ecommerce: Noteworthy trends in retail for the present and future