Pioneer Institute Expects That Massachusetts Taxpayers Will Be Refunded $3.2B Due To State Revenue Cap

Pioneer Institute projects that the state will refund approximately $3.2 billion to taxpayers due to a state law sponsored by Citizens for Limited Taxation and voted on by taxpayers in 1986 that caps the amount of revenue the state can collect in any given year.

Under the cap, state revenues are limited based on the average growth of wages and salaries during the previous three years. While the Department of Revenue has disclosed collections through May, the state’s fiscal year ended on June 30 and June revenues are not yet available. To estimate the refund to taxpayers, Pioneer replicated the calculations prepared by the state auditor in prior years to determine if a refund was due and estimated June revenue based on historic trends.

The state auditor is required by law to perform the calculation annually based on information supplied by the Department of Revenue. This is the first time in decades the state will return money to the taxpayers.

“We’ve hit a tipping point where Massachusetts taxpayers have maxed out their obligations to fund state government,” said Pioneer Institute Executive Director Jim Stergios. “The lesson is: stable tax laws allow the economic growth that generates these giant government surpluses. So why are we even considering tax hikes?”

Get Updates on Our Economic Opportunity Research

Related:

https://pioneerinstitute.org/wp-content/uploads/Pioneer-Institute-Statement-on-Question-1.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-11-09 16:09:302022-11-09 16:09:30Pioneer Institute Statement on Question 1

https://pioneerinstitute.org/wp-content/uploads/Pioneer-Institute-Statement-on-Question-1.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-11-09 16:09:302022-11-09 16:09:30Pioneer Institute Statement on Question 1 https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-29 11:28:502022-07-29 11:28:50Pioneer Institute Expects That Massachusetts Taxpayers Will Be Refunded $3.2B Due To State Revenue Cap

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-29 11:28:502022-07-29 11:28:50Pioneer Institute Expects That Massachusetts Taxpayers Will Be Refunded $3.2B Due To State Revenue Cap https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-2-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-06 07:49:072022-07-06 07:54:29Survey of Business Sentiment: MA Income Tax Hike Would Lead to Employer Exodus

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-2-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-07-06 07:49:072022-07-06 07:54:29Survey of Business Sentiment: MA Income Tax Hike Would Lead to Employer Exodus https://pioneerinstitute.org/wp-content/uploads/Picture1-2.png

247

624

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

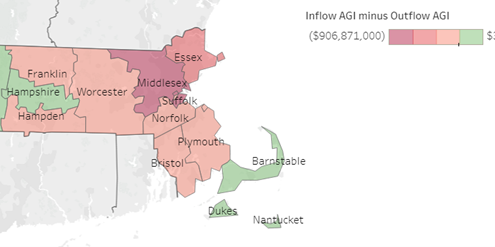

Editorial Staff2022-06-09 10:58:442022-06-09 10:59:08As States Compete for Talent and Families, Massachusetts Experienced a Six-Fold Increase in Lost Wealth Compared to a Decade Earlier

https://pioneerinstitute.org/wp-content/uploads/Picture1-2.png

247

624

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-06-09 10:58:442022-06-09 10:59:08As States Compete for Talent and Families, Massachusetts Experienced a Six-Fold Increase in Lost Wealth Compared to a Decade Earlier https://pioneerinstitute.org/wp-content/uploads/Untitled-design-2022-05-25T083008.246.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-05-25 08:30:492022-07-06 07:51:30Book Reveals How Tax Hike Amendment Would Damage Commonwealth’s Economic Competitiveness

https://pioneerinstitute.org/wp-content/uploads/Untitled-design-2022-05-25T083008.246.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-05-25 08:30:492022-07-06 07:51:30Book Reveals How Tax Hike Amendment Would Damage Commonwealth’s Economic Competitiveness https://pioneerinstitute.org/wp-content/uploads/public-statement-1.png

900

1600

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-27 11:57:102022-01-28 11:24:17Pioneer Supports Legal Challenge to Misleading Tax Ballot Language, Releases Video

https://pioneerinstitute.org/wp-content/uploads/public-statement-1.png

900

1600

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-27 11:57:102022-01-28 11:24:17Pioneer Supports Legal Challenge to Misleading Tax Ballot Language, Releases Video https://pioneerinstitute.org/wp-content/uploads/Understatement-web-post.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-18 06:52:502022-01-18 06:58:42Study: Tax Up For A Vote In November Would Ensnare Over Three Times More Taxpayers Than Previously Estimated

https://pioneerinstitute.org/wp-content/uploads/Understatement-web-post.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-01-18 06:52:502022-01-18 06:58:42Study: Tax Up For A Vote In November Would Ensnare Over Three Times More Taxpayers Than Previously Estimated