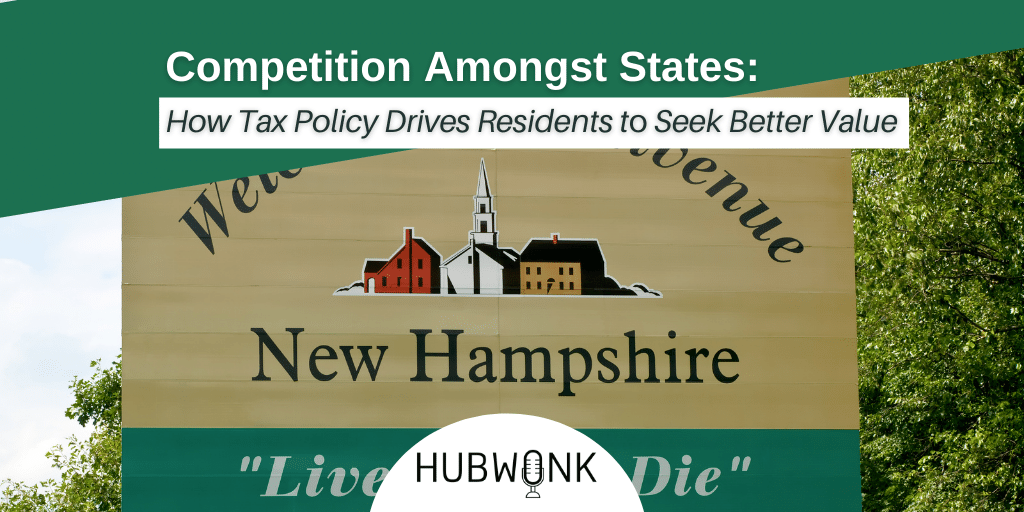

Competition Amongst States: How Tax Policy Drives Residents to Seek Better Value

This week on Hubwonk (our debut video & audio edition), Host Joe Selvaggi talks with research analyst Andrew Mikula about the findings from his recent report, A Timely Tax Cut, in which he explored the relationship between state tax rates and policy and the direction of interstate migration.

Guest

Andrew Mikula is a former Economic Research Analyst at Pioneer Institute and current candidate for a Master’s in Urban Planning at Harvard University.

Get new episodes of Hubwonk in your inbox!

Read a Transcript of This Episode:

Please excuse typos.

Joe Selvaggi (00:00):

This is Hubwonk, I’m Joe Selvaggi

Joe Selvaggi (00:09):

Welcome to Hudwonk, a podcast of Pioneer Institute, a think tank in Boston. A natural consequence of being a nation of united individual states is that it creates 50 different laboratories of democracy. Each state decides how best to serve its citizens and in turn, by what means it will tax its citizens to pay for those services. The state prerogative to tax and spend has the benefit of creating competition among states to attract more tax paying residents with its value proposition. While a high tech state can assert it offers better services and a low-tech state can lay claim to lower cost of living the arbiter of a state’s value or the people themselves. All citizens can pick candidates in elections. A far more powerful way to express a preference is to optimize great from one state to another, bringing with you all future taxable income, the effect of this migration in the long run.

Joe Selvaggi (01:05):

It can be either to boost the state’s tax base or drain it of its vital revenue. How well is Massachusetts competing with this neighbor states and how are changes in tax law, such as the proposed millionaire’s tax likely to affect the movement of those with higher income who invest in and create new companies in the future? My guest today is Andrew Mikula, former research analyst of Pioneer Institute and current graduate student at Harvard’s graduate school of design. Andrew’s most recent research paper, a timely text that how New Hampshire is taking advantage of Massachusetts graduated income tax proposal maps, current interstate migration, and looks for a correlation between state tax levels and the direction of income flows. Andrew shares with us the findings of his paper and provides color on why residents may vote with their feet. When I return, I’ll be joined by research analyst, Andrew Mikula.

Joe Selvaggi (02:52):

Okay. We’re back. This is Hubwonk, I’m Joe Selvaggi and I’m now joined by Pioneer Institute’s former economics researcher and current Harvard graduate school of design master’s degree student Andrew Mikula. Welcome back to Hubwonk, Andrew.

Andrew Mikula (03:06):

Joe, thanks so much for having me back.

Joe Selvaggi (03:09):

Well, first let me congratulate you on starting your master’s degree in urban planning. I believe. How have your studies been going so far?

Andrew Mikula (03:15):

It’s going well. Yeah, a lot of requirements this semester, but we’ll get to the juicy stuff soon. And it’s an important foundation.

Joe Selvaggi (03:25):

Well, I am, I’m thrilled that you were able to take some time out of your studying to be with us. I want to explore the findings of your newest research paper, entitled a timely tax cut, how New Hampshire is taking advantage of Massachusetts graduated income tax proposal. All right. We’ve covered this topic in different ways in the past on how long, but I want to give the listeners and viewers now we’re viewing we’re now recording the visual of our, of our show. I want to give everyone some background on tax rates, what’s being proposed. What are the relative tax rates in Massachusetts and New Hampshire? Let’s start with Massachusetts. We used to be known as Taxachusetts. Where are we now?

Andrew Mikula (04:04):

Right. So I think in importantly, for our purposes of voters passed a ballot measure in the year 2000, that would lower the income tax rate from 5.9 to 5.0% over the next three years. It was later tied to benchmarks and revenue growth slowing down the tax cuts are that it only reached 5.0% last year, actually in 2020. Okay. so I think that we’ve taken a kind of incremental approach, but we have cut income taxes in recent years. New Hampshire has had a 5% tax on interest in dividends for a while, but what they don’t tax is wage income, right? So it’s only the interest in dividends you would earn on a financial asset that are, are taxed. At least for individuals, corporations is a different matter. But the tax rate is 5% on interest in dividends. Like it is Massachusetts today.

Joe Selvaggi (05:08):

Okay. So that seems like a stark contrast. We have 5% on income here, Massachusetts. So that’s the lowest has been for a while. It just got to 5% recently. But that’s a flat tax for everyone, every dollar earned in Massachusetts tax at that 5% rate in New Hampshire, it’s zero. They do tax some income that comes from interest in dividends, but not from income. So that seems like a pretty stark difference. I want to get to a different aspect of, of the tax code. I, I mentioned that ours is a flat tax rate. Your paper talks about a proposal for a graduated rate. I’m fairly sure we have a federal tax rate that is graduated, but explain to our listeners, what does that mean? What do we have now flat and what what is being proposed

Andrew Mikula (05:52):

That’s right. So the rate itself, Massachusetts levy is in terms of income, personal income taxes, 5% is, is relatively on par with the average for state governments. What’s relatively uncommon is we have a flat tax. So we tax people at 5% of their income, regardless of if they’re making, you know, 40,000 a year or 400,000 a year. And that’s so in the, especially in the context of the Northeast, that makes us pretty unique actually.

Joe Selvaggi (06:28):

So I’m graduate Texas sounds like people who have more money might pay a higher rate. I want to talk about the, sort of the one aspect of raising taxes is raising taxes on everyone is unpopular. I would say the flat tax does have the benefit of, of constraining legislators inclined to raise taxes by it’s very hard to raise taxes on everyone. To me, graduated income taxes, seem a bit like a divide and conquer. We identify a group we’d like to raise the taxes on and every everyone votes yes. To vote to tax the other guy. Do I have a good sense of the power of a graduated tax?

Andrew Mikula (07:09):

Yeah, you, you do Joan, no one thinks that, you know, someone else can spend their money more effectively or better than, than they can, but it’s appealing that to take a small segment of the population and say, they’re going to be paying more because they’re not paying enough now. And the rest of the people are going to accrue the benefits in terms of, you know, public services. I think where that gets complicated is in part the effect on, on the revenue volatility that comes with, you know, having a tax, that’s not quite as broad-based as say a sales tax. And so, you know, income taxes have been shown to lead to, you know, kind of steeper drops in some tax revenue collections, and as a whole during recessions especially the great recession actually,

Joe Selvaggi (08:17):

Okay. So I want to drill down a little more into what we mean by graduated tax. It means we’re, we’re texting higher income people at a higher rate in general and lower income people at a lower rate who, or what is being proposed in Massachusetts, what is this so-called millionaire’s tax and what is it to rate?

Andrew Mikula (08:37):

Right? So the proposal in Massachusetts would levy a 4% surtax on annual personal income, over a million dollars. That’s both wage income, capital gains you know, he’s selling a business, et cetera. And this proposal has a really interesting history. It was, it’s a pretty bottom up proposal, but it was actually struck down by the Massachusetts Supreme judicial court in, in 2018 before being rekindled as a legislative petition the following year and changing the Massachusetts constitution which this tax would do is a very iterative process. And so it’s, it’s not going on the statewide ballot until the fall of 2022 and voters have a chance to weigh in before it’s signed into law.

Joe Selvaggi (09:37):

So we sh we shouldn’t panic right now. This is something that’s coming, as you say, from, from the bottom up, actually from the legislator. So where did it start? Well, let me take a step back. We have a 5% income tax now and we’ve just gone through a recession through a epidemic that had a slight recession the economy shut down for a time. And there was a lot of concern that with the, a depressed economy, you would be a depressed revenue flow. I’ve read that the state has actually had a surplus of revenue. In fact, they surprise to the upside on revenue. Is, do you see this interest in raising the tax rate on millionaires being driven by a need for revenue? Is there a need for revenue in Massachusetts right now?

Andrew Mikula (10:28):

Right. So like I alluded to, you know, this proposal has been on the table since 2015 or so, so I’m not sure it’s, it’s accurate to argue that this is, you know, the reason why this proposal was put forward is not because of the pandemic. Right. but I also think that you know, we we’ve, there were some temporary impacts on the state revenues from COVID, but our, our bounce back has been much quicker than in the great recession, right? Because the, the economic recession that we’ve had because of COVID reflects the presence of the virus whose presence has wavered, you know, a lot over the course of the last year and a half, whereas, you know, kind of more deep rooted problems with our financial system characterized or caused much of the previous recessions wolves. And so it’s true that currently Massachusetts tax collections are, are essentially at record highs in a lot of major categories. And on top of that, we have a large amount of federal stimulus dollars still to spend in the base state. So I think one argument that opponents of the tax hike make is that we don’t meet, we don’t necessarily need this added revenue right now in kind of an urgent way. That’s true.

Joe Selvaggi (12:12):

That’s fair. So I’ll accept that if this has been coming down the line since 2015 and the economic situation has sometimes been better, sometimes been worse. It’s not really motivated by an immediate need for revenue, but rather a, perhaps a longterm desire for additional revenue to be spent at the state level. So let’s take it out of the current events and say, okay, this is the long-term direction of Massachusetts. We’d like to tax those who make more than a million dollars at a higher rate than those who make less than a million dollars. But let’s talk about then let’s shift to the focus of your paper which doesn’t just merely look at the relative tax rates of New Hampshire and Massachusetts. It talks about some other states and their relative tax rates, but the crux of your paper talks about what I like to call the Footloose nature of the individuals within each state that is, each of us has a choice as to which state we want to live in. And sometimes tax rates have an influence on who moves, where tell us from a 10,000 feet view, what your conclusions or your observations were on the relationship between the relative tax rate of a state and the relative inflow or outflow of higher earners to those states.

Andrew Mikula (13:23):

Yeah. Let me say, you know, the tax cut in New Hampshire combined with Massachusetts is a legislative initiative here or constitutional amendment, really. I think some folks are concerned that it will lead to, you know a decrease in economic activity, decreased of investment in Massachusetts are making it harder or less economical to create jobs and invest in businesses. So we can actually measure how the tax bases of certain states are changing because of people moving from one state to another, in a given year. And that’s exactly what I’ve done in this paper. You can see on a graph that in a lot of cases, capital flows between a given pair of states correspond quite closely to changes in tax policy in those states. And, you know, it doesn’t necessarily flip the sign right away in which a state is the risk net receiver of more of those tax dollars, but it’s a long-term effect that plays out over 10 or 15 years, which is one thing that makes, you know, tax proposals like this. So insidious,

Joe Selvaggi (14:49):

Yeah, I was struck by your paper. You do quantify those outflows. And when we talk about this is before any changes, either the ones in Massachusetts currently proposed, or the ones in New Hampshire proposed but in 2019 two years ago, the outflow of income from Massachusetts to New Hampshire in one year was $426 million outflow from Massachusetts to New Hampshire. Now we can’t know the motive for moving north, but it can’t, it can’t be the weather. W what are your thoughts? How is it that, you know it is the tax rate. Is there any other confounding factor that you think might contribute to people moving out of Massachusetts towards New Hampshire?

Andrew Mikula (15:32):

Absolutely. I, you know, taxes are a part of the story, but I think a big one is the cost of living and new Hampshire’s tax rates, you know, on wage income at least have been zero for as long as I can remember. But, you know, even when you, when you start cutting Massachusetts as tax rates, as we have done the past 20 years, there’s still this, this gap here, you know, New Hampshire was not New Hampshire has not been sending folks to Massachusetts on net, as long as we’ve been keeping track of the IRS has been keeping track. So, and I think you’d also see that kind of cost of living cost of housing concern and start to creep in, and places like Rhode Island, Rhode Island has, you know, cut taxes more aggressively than we have in the past, you know, 10 or 15 years.

Andrew Mikula (16:28):

But there are certainly other factors in the mix because, you know, we can see that, you know, people are on net moving from Massachusetts to Rhode Island. And despite their changes in the tax code, the, the top marginal tax rate in Rhode Island is still higher than it is here. So it’s, it’s, it’s really interesting to see how, you know, oftentimes you need to go deeper than just the, you know, headline tax rate and understand how changes in tax rates over time can affect things, because people are also taking into account things like the cost of living and family connections and job growth, et cetera.

Joe Selvaggi (17:09):

I think it’s worth mentioning also a you talk about the cost of living. I think those who assume are higher tax rate means better services, perhaps better schools or better roads, better bridges infrastructure. I’ve been to New Hampshire. It’s less than an hour away in a car from downtown Boston. There bridges and roads look fine to me. Do they have problems with services and frankly, if you have the data, how do they collect revenue to support their state’s requirements?

Andrew Mikula (17:38):

Yeah, so New Hampshire does kind of conform to some of the kind of low tax state paradigms, and that it, it spends a lot less than Massachusetts on a per capita basis. I’d also say that New Hampshire has, you know, the lowest poverty rate in the country. So compared to, you know, how much, if you’re, if your goal is to provide a certain base level of, of services that ensure a certain quality of life, New Hampshire might not have the same needs as most other states and Massachusetts is, is a low poverty state too. But I think it also is, is less than modernist than New Hampshire in terms of socioeconomic status. That said, I think a lot of the difference in terms of the level of spending between New Hampshire and Massachusetts still reflects policy differences, not just different needs, New Hampshire is the only state east of the Mississippi that doesn’t provide some sort of public preschool. They’re also pretty strict about time costs for services to the people using those services. You know, higher education in New Hampshire is largely funded by tuition, as opposed to transfers from the state general fund pension funds for state workers are mostly funded by the workers’ salaries while they’re working as opposed to regular contributions from the state. And there are several examples of that sort of cost cutting measure that has a state, the state money.

Joe Selvaggi (19:24):

So it’s a we, we believe in a Federalist system. So you have different states with different needs and different priorities. So you, you make a great case if there’s more to the story than just a marginal tax rates at the state level. I, I appreciate that. Let’s talk about the the millionaire’s tax, the additional 4% tax on those earning more than a million dollars, there are going to be the ones who are affected, and they’re the ones who are likely to potentially vote with their feet. What’s the profile of someone who earns more than a million dollars in a year. Is it a rich banker or is it someone else,

Andrew Mikula (19:59):

Right? Well, I think, you know, there may be a fair share of rich bankers, but prior work that pioneer has conducted has also shown that, that, you know, a large plurality of the people who, you know, make a million dollars in a year in a given 10 year period or so do so only once that’s based on IRS data. And I think that’s a fairly good indicator that a lot of these people are cashing out on investments they’ve made so that they can either retire or they’re selling a business or a home, or what have you. And so I think an ostensible goal of a new Hampshire’s policy here was to in cutting the interest in dividends tax was to lower the tax burden on some older people and also attract more taxpayers that are, are going to consume a lot in New Hampshire and pay a lot in property taxes as well. But I think it’s more complicated than just, you know, there’s a banker there’s, you know, a real estate developer, et cetera.

Joe Selvaggi (21:26):

So you’re, that’s a very interesting piece of data. We’ve covered it a bit on hub Blanca in the past. So people who earn a million dollars in general and over 10 year period, do it only once, which suggests they’re not earning an income and a salary more than a million dollars, but rather it’s what we would call a liquidity event. They’ve sold a house, they sold a business, something that perhaps they’ve built over the course of their lifetime, and they want to essentially cash out, perhaps retire, perhaps do something else. But even if it is bankers, isn’t it people who are creating businesses by investing and hoping to profit from taking some risks and investing. In other words, isn’t it people who are creating businesses and creating jobs that are most apt to be effected by a tax on ultimately their, their success, their ultimate cash out.

Andrew Mikula (22:13):

Right. And I think that’s, you know, that very reason is, has been one of the strongest arguments in the past for either reducing income taxes or looking for, you know, alternative ways of taxing the economic activity that comes out of a place. And I think the, the, you know, the economic literature might be divided about how exactly to implement something like this, but there is evidence that, that state level of taxes on income well tend to reduce incentives to earn income. And, you know, that’s something we need to weigh against other forms of taxation that have different effects sales or consumption-based taxes might overly burden certain people, depending on, on what they’re buying property taxes might be hard to avoid in the short term might be relatively stable even during recessions when a lot of people are out of work. So it’s a trade off that I think you know Warren, some more discussion, but in general, I’d say, you know, people like earning income taxing it is means less income, less work, less investment for in, into the economy.

Joe Selvaggi (23:57):

Yes. you know, I, it seems intuitively obvious that you tax something, you’d get less of it. I think policy makers understand let’s say, in the form of sin taxes they tax tobacco or alcohol with the stated goal of trying to reduce its use. It seems to follow that taxing income would either make people choose to have to be compensated differently, or take their income with them to a place where it’s taxed less. Out of curiosity, does it, in fact, New Hampshire tax it must raise revenue in other forms it’s in the form of consumption tax, I guess, sales tax and property tax is that how they raise their revenue in New Hampshire?

Andrew Mikula (24:41):

Largely. So they actually also have some higher business taxes and we do in Massachusetts, but you’re right, that instead of a broad-based sales tax, they have some, you know, more targeted excise taxes. And also one thing that’s pretty unique about New Hampshire is they also have state owned you know, kind of stores that do a lot of business to out-of-state customers. And a famous example is the slew of liquor stores that are right over the Massachusetts border that you know, the technically are not taxed, but it’s New Hampshire collecting that sales revenue. And that’s helped explain how almost 20% of new Hampshire’s kind of unrestricted revenue in a given year actually comes from some of these sin taxes or other excise taxes.

Joe Selvaggi (25:52):

Good. So a Massachusetts pays its own income taxes and it pays some new Hampshire’s alcohol taxes. Is that right for helping New Hampshire make ends meet with our, when we drive north to to the state run a liquor store,

Andrew Mikula (26:08):

Essentially. Yes. You know, it’s this sort of paradigm where New Hampshire draws out of state customers to essentially pay its tax bills is already happening on the kind of consumption side of things

Joe Selvaggi (26:27):

I enjoyed in your PC. You didn’t just talk about New Hampshire and Massachusetts, as we’ve talked a little bit about the Connecticut Rhode Island we’ve had inflows from those two states. I was amazed to learn you even tracked New York and New Jersey. We’ve had substantial inflows from those states as well because they have substantially higher income tax on high net worth individuals, $200 million, roughly from each Massachusetts from New York and New Jersey respectively. That’s an impressive number. Would you conclude then that New Hampshire and New York also decamped from those locations largely because of the relative tax rates or are there other confounding issues in those, in those cases?

Andrew Mikula (27:14):

Yeah, I think that’s certainly part of it. You know, there are even in, in some parts of New York, you know, you could make more bang for your buck argument in Massachusetts cost of living wise. But I think what’s really striking to me is in the case of New York, you know, it used to be that, that more, you know, adjusted gross income from migrating taxpayers was going from Massachusetts to New York. And then some point in the mid two thousands, you know, it changed sign. And in 2019, it’s, you know, $170 million that migrating new Yorkers are adding to our tax base every year.

Joe Selvaggi (28:04):

So that’s substantial. And again there are two very, very wealthy states with high services. So really the, the major variable there between, let’s say, New York city and Metro Boston, if you will, if you will is cost of living in primarily income tax.

Andrew Mikula (28:23):

Hmm. I’m also fascinated. I think it’s still kind of, we’re still kind of in this weird limbo with what effect the, or how long-term the remote work revolution will last, which I think can certainly impact whether someone’s willing to, you know, pack up and move to New Hampshire and, and have a longer commute to work. But you know, it’s New York has certainly been hit harder than most states in that regard. So it’s going to be especially interesting to follow the tax flows between New York and Massachusetts in recent, in upcoming years.

Joe Selvaggi (29:06):

That’s very interesting. We didn’t really talk about it too much, but we did, we have talked in past, have long episodes that COVID really made us aware of the fact that we could remote work remotely. And if you want to live in New Hampshire and enjoy the lower income tax and you work in Boston, it’s a heck of a commute. And if you only have to do that three days a week, instead of five days a week, you may be more inclined to explore moving to New Hampshire. Is that what you’re saying?

Andrew Mikula (29:35):

Yeah. Yeah, absolutely.

Joe Selvaggi (29:38):

Wonderful. All right. So we’re getting close to the end of our time. I, I appreciate you taking time with me. How can our listeners and new viewers find your paper, read more about your work and and see the graphs for themselves.

Andrew Mikula (29:54):

It’s all@pioneerinstitute.org is our recent work. We do a lot of research and do tax policy and, and broader economic opportunity issues. Thanks so much for having me, Joe.

Joe Selvaggi (30:06):

I appreciate your time, Andrew, and best of luck with your studies. I hope you enjoy it.

Joe Selvaggi (30:13):

This has been another episode of Hubwonk, a podcast of Pioneer Institute, a think tank in Boston. If you enjoyed today’s show, there are several ways to support us. It will be easier for you and better for us. If you subscribe to Hubwonk on iTunes, if you’d like to help others find Hubwonk, it would be great if you would offer a five-star rating or a favorable review, it’s always welcome. If you’d like to share Hubwonk with friends. If you have ideas for me, or comments or suggestions for topics for future episodes, you’re welcome to email me at hubwonk@pioneerinstitute.org. Please join me next week for a new episode of Hubwonk

Check out our most recent episodes:

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-210-Michelle-07232024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-23 11:02:462024-07-23 11:27:12Registering Republican Realignment: GOP Convention Showcases Conservatism’s New Direction

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-210-Michelle-07232024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-23 11:02:462024-07-23 11:27:12Registering Republican Realignment: GOP Convention Showcases Conservatism’s New Direction https://pioneerinstitute.org/wp-content/uploads/Hubwonk-209-Eide-07162024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-16 16:53:482024-07-16 16:53:48Candidate Selection Breakdown: Presidential Primary Primacy or Determined Delegate Detour

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-209-Eide-07162024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-16 16:53:482024-07-16 16:53:48Candidate Selection Breakdown: Presidential Primary Primacy or Determined Delegate Detour https://pioneerinstitute.org/wp-content/uploads/Hubwonk-208-Eide-07092024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-09 11:19:352024-07-09 11:20:26Breaking Down Encampments: Court Finds no Right to Sleep Outdoors

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-208-Eide-07092024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-09 11:19:352024-07-09 11:20:26Breaking Down Encampments: Court Finds no Right to Sleep Outdoors https://pioneerinstitute.org/wp-content/uploads/Hubwonk-207-SMith-07022024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-02 10:42:272024-07-02 10:44:39Underfunding Overdose Alternatives: Price Controls Hinder Search for Non-Addictive Opioids

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-207-SMith-07022024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-02 10:42:272024-07-02 10:44:39Underfunding Overdose Alternatives: Price Controls Hinder Search for Non-Addictive Opioids https://pioneerinstitute.org/wp-content/uploads/Hubwonk-204-Mikula-06252024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-25 10:51:302024-06-25 10:51:30Unlocking Affordable Housing: Sources and Solutions for Cost Crisis

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-204-Mikula-06252024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-25 10:51:302024-06-25 10:51:30Unlocking Affordable Housing: Sources and Solutions for Cost Crisis https://pioneerinstitute.org/wp-content/uploads/Hubwonk-204-Berry-06182024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-18 12:09:292024-06-18 12:09:29Jawboning Free Speech: State Coercion Finds Limits at Supreme Court

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-204-Berry-06182024-.png

432

767

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-18 12:09:292024-06-18 12:09:29Jawboning Free Speech: State Coercion Finds Limits at Supreme Court https://pioneerinstitute.org/wp-content/uploads/Hubwonk-204-Packard-06112024-.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-11 10:48:392024-06-11 10:48:39Protectionism’s Bipartisan Embrace: Who Pays When Imports Cost More

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-204-Packard-06112024-.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-11 10:48:392024-06-11 10:48:39Protectionism’s Bipartisan Embrace: Who Pays When Imports Cost More https://pioneerinstitute.org/wp-content/uploads/Hubwonk-203-Michel-05282024-Pioneer-Post.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-04 11:15:502024-06-04 11:31:45Universal Savings Accounts: Designing Tax Incentives that Pay to Save

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-203-Michel-05282024-Pioneer-Post.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-04 11:15:502024-06-04 11:31:45Universal Savings Accounts: Designing Tax Incentives that Pay to Save