https://pioneerinstitute.org/wp-content/uploads/MBTA-Subway-Returns-Feature.jpg

450

600

Eamon McCarthy Earls

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eamon McCarthy Earls2019-04-01 16:48:532021-10-29 15:18:12MBTAAnalysis: A look inside the MBTA

https://pioneerinstitute.org/wp-content/uploads/MBTA-Subway-Returns-Feature.jpg

450

600

Eamon McCarthy Earls

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eamon McCarthy Earls2019-04-01 16:48:532021-10-29 15:18:12MBTAAnalysis: A look inside the MBTA https://pioneerinstitute.org/wp-content/uploads/CloseupClock-1.jpg

739

1244

Mary Connaughton

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Mary Connaughton2017-02-20 12:34:192017-02-21 09:47:58The Clock is Ticking…….

https://pioneerinstitute.org/wp-content/uploads/CloseupClock-1.jpg

739

1244

Mary Connaughton

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Mary Connaughton2017-02-20 12:34:192017-02-21 09:47:58The Clock is Ticking……. https://pioneerinstitute.org/wp-content/uploads/Screenshot-2024-10-06-204348.png

488

736

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-10-06 21:12:052024-10-07 11:34:13Pioneer Institute Study Finds Wide Range of Approaches to Compliance with MBTA Communities Law

https://pioneerinstitute.org/wp-content/uploads/Screenshot-2024-10-06-204348.png

488

736

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-10-06 21:12:052024-10-07 11:34:13Pioneer Institute Study Finds Wide Range of Approaches to Compliance with MBTA Communities Law https://pioneerinstitute.org/wp-content/uploads/Monthly-Musings-June-1.png

475

717

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-29 15:37:292024-07-29 15:41:06Pioneer Institute Statement on the Project Labor Agreement Provision in the Massachusetts Economic Development Bill

https://pioneerinstitute.org/wp-content/uploads/Monthly-Musings-June-1.png

475

717

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-29 15:37:292024-07-29 15:41:06Pioneer Institute Statement on the Project Labor Agreement Provision in the Massachusetts Economic Development Bill https://pioneerinstitute.org/wp-content/uploads/Op-ed-Schedule-A-Enright-01292024.png

1400

1400

Aidan Enright

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Aidan Enright2024-01-29 15:39:002024-08-01 07:01:40Skill-based immigration could ease labor shortage

https://pioneerinstitute.org/wp-content/uploads/Op-ed-Schedule-A-Enright-01292024.png

1400

1400

Aidan Enright

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Aidan Enright2024-01-29 15:39:002024-08-01 07:01:40Skill-based immigration could ease labor shortage https://pioneerinstitute.org/wp-content/uploads/Benefit-Cliffs-Paper-11062023.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-11-06 09:00:562023-11-03 16:06:46New Report Explores Impact of Welfare Benefit Cliffs

https://pioneerinstitute.org/wp-content/uploads/Benefit-Cliffs-Paper-11062023.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-11-06 09:00:562023-11-03 16:06:46New Report Explores Impact of Welfare Benefit Cliffs https://pioneerinstitute.org/wp-content/uploads/Lottery-Featured-Image.jpg

683

1024

Peter Mentekidis

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Peter Mentekidis2023-06-06 15:05:372023-06-06 15:05:37The MassLottery: A Bay Stater’s Favorite Pastime

https://pioneerinstitute.org/wp-content/uploads/Lottery-Featured-Image.jpg

683

1024

Peter Mentekidis

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Peter Mentekidis2023-06-06 15:05:372023-06-06 15:05:37The MassLottery: A Bay Stater’s Favorite Pastime https://pioneerinstitute.org/wp-content/uploads/work-force.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-05-02 09:11:232023-05-03 15:37:07Study Finds Massachusetts Workforce Has Become More Female, Older, More Diverse

https://pioneerinstitute.org/wp-content/uploads/work-force.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-05-02 09:11:232023-05-03 15:37:07Study Finds Massachusetts Workforce Has Become More Female, Older, More Diverse https://pioneerinstitute.org/wp-content/uploads/Nail-salons-image.webp

574

907

Charles Chieppo

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Charles Chieppo2023-02-22 15:11:052024-08-01 06:51:10Licensing burdens thwart economic growth in Massachusetts

https://pioneerinstitute.org/wp-content/uploads/Nail-salons-image.webp

574

907

Charles Chieppo

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Charles Chieppo2023-02-22 15:11:052024-08-01 06:51:10Licensing burdens thwart economic growth in Massachusetts https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-10.png

512

1024

Tom Ahn

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Tom Ahn2022-09-21 10:11:192022-09-21 10:11:19What We Do and Don’t Know about Online Platform Rideshare/Delivery Workers in Massachusetts

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-10.png

512

1024

Tom Ahn

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Tom Ahn2022-09-21 10:11:192022-09-21 10:11:19What We Do and Don’t Know about Online Platform Rideshare/Delivery Workers in Massachusetts https://pioneerinstitute.org/wp-content/uploads/Untitled-design-2022-05-25T083008.246.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-05-25 08:30:492022-07-06 07:51:30Book Reveals How Tax Hike Amendment Would Damage Commonwealth’s Economic Competitiveness

https://pioneerinstitute.org/wp-content/uploads/Untitled-design-2022-05-25T083008.246.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-05-25 08:30:492022-07-06 07:51:30Book Reveals How Tax Hike Amendment Would Damage Commonwealth’s Economic Competitiveness https://pioneerinstitute.org/wp-content/uploads/public-statement-zoning.png

900

1600

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2022-04-11 10:03:442022-04-11 10:03:44A Vision for Sustainable, Transit-oriented Development

https://pioneerinstitute.org/wp-content/uploads/public-statement-zoning.png

900

1600

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2022-04-11 10:03:442022-04-11 10:03:44A Vision for Sustainable, Transit-oriented Development https://pioneerinstitute.org/wp-content/uploads/FareEvasionWeb.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2022-01-18 14:21:482022-01-19 06:14:19The MBTA’s Looming Bus and Green Line Fare Evasion Crisis

https://pioneerinstitute.org/wp-content/uploads/FareEvasionWeb.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2022-01-18 14:21:482022-01-19 06:14:19The MBTA’s Looming Bus and Green Line Fare Evasion Crisis https://pioneerinstitute.org/wp-content/uploads/Understatement-web-post.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2022-01-18 06:57:312022-01-18 07:02:03The Great Understatement: Far more taxpayers and businesses than previously estimated will be affected by the proposed surtax

https://pioneerinstitute.org/wp-content/uploads/Understatement-web-post.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2022-01-18 06:57:312022-01-18 07:02:03The Great Understatement: Far more taxpayers and businesses than previously estimated will be affected by the proposed surtax https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-11-17 05:48:072021-11-17 05:48:07The Far-Reaching Impact of a Massachusetts Surtax: Anecdotal Evidence and Data Analysis

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-1.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-11-17 05:48:072021-11-17 05:48:07The Far-Reaching Impact of a Massachusetts Surtax: Anecdotal Evidence and Data Analysis https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-10-07 06:10:092021-10-07 06:10:09A Timely Tax Cut: How New Hampshire is Taking Advantage of Massachusetts’ Graduated Income Tax Proposal

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-12.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-10-07 06:10:092021-10-07 06:10:09A Timely Tax Cut: How New Hampshire is Taking Advantage of Massachusetts’ Graduated Income Tax Proposal https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-11.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-09-27 05:37:012021-09-27 05:42:53The SALT Cap: An Accelerator for Tax Flight from Massachusetts

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-11.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-09-27 05:37:012021-09-27 05:42:53The SALT Cap: An Accelerator for Tax Flight from Massachusetts https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-1-4.png

512

1024

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Nina Weiss2021-08-10 05:35:072021-08-10 05:37:24PILOT Agreements: Nonprofits’ Fair Portion or Government Extortion?

https://pioneerinstitute.org/wp-content/uploads/WordPress-Blog-Post-Featured-Image-1-4.png

512

1024

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Nina Weiss2021-08-10 05:35:072021-08-10 05:37:24PILOT Agreements: Nonprofits’ Fair Portion or Government Extortion? https://pioneerinstitute.org/wp-content/uploads/Tax-Flight-Photo-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-06-17 05:24:472021-06-17 05:24:47Tax Flight of the Wealthy: An Academic Literature Review

https://pioneerinstitute.org/wp-content/uploads/Tax-Flight-Photo-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-06-17 05:24:472021-06-17 05:24:47Tax Flight of the Wealthy: An Academic Literature Review https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-06-01 05:56:112021-06-01 05:56:29Are Massachusetts taxes regressive? A common argument for a graduated income tax relies on a deeply flawed and outdated study

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-06-01 05:56:112021-06-01 05:56:29Are Massachusetts taxes regressive? A common argument for a graduated income tax relies on a deeply flawed and outdated study  https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-05-05 05:31:342021-12-29 12:17:37The Big Lure: Interstate Competition Exacerbates the Economic Fallout from Telecommuting Trends

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-05-05 05:31:342021-12-29 12:17:37The Big Lure: Interstate Competition Exacerbates the Economic Fallout from Telecommuting Trends https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-5.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-28 14:59:382021-11-23 10:55:03Statement before the MA Joint Committee on Revenue in Opposition to HB 86 (Pages 1-4) A legislative amendment to the Constitution to provide resources for education and transportation through an additional tax on incomes in excess of one million dollars.

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-5.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-28 14:59:382021-11-23 10:55:03Statement before the MA Joint Committee on Revenue in Opposition to HB 86 (Pages 1-4) A legislative amendment to the Constitution to provide resources for education and transportation through an additional tax on incomes in excess of one million dollars. https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

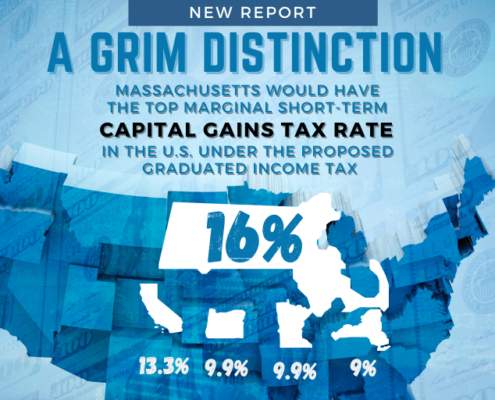

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-04-26 05:05:452021-12-29 12:24:00A Grim Distinction: Massachusetts would have top marginal short-term capital gains tax rate in the U.S. under the proposed graduated income tax

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-04-26 05:05:452021-12-29 12:24:00A Grim Distinction: Massachusetts would have top marginal short-term capital gains tax rate in the U.S. under the proposed graduated income tax https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Nina Weiss2021-04-20 05:38:152021-11-23 10:25:38The Graduated Income Tax Trap: A Tax on Small Businesses

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Nina Weiss

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Nina Weiss2021-04-20 05:38:152021-11-23 10:25:38The Graduated Income Tax Trap: A Tax on Small Businesses https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-3.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-04-07 05:36:462021-11-23 10:34:15The Great Mismatch: The graduated income tax proposal’s gravely flawed escalation factor

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-3.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-04-07 05:36:462021-11-23 10:34:15The Great Mismatch: The graduated income tax proposal’s gravely flawed escalation factor https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-04-01 05:49:202021-11-23 10:52:41The Graduated Income Tax Trap: A retirement tax on small business owners

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-04-01 05:49:202021-11-23 10:52:41The Graduated Income Tax Trap: A retirement tax on small business owners https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-03-25 05:34:372021-12-29 12:19:26Missing the Mark on Wealth Migration: Past Studies Drastically Undercounted Millionaires

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-03-25 05:34:372021-12-29 12:19:26Missing the Mark on Wealth Migration: Past Studies Drastically Undercounted Millionaires https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster.png

512

1024

Serena Hajjar

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Serena Hajjar2021-03-15 05:31:572021-03-15 05:31:57Public vs. Private Employment in Massachusetts: A Tale of Two Pandemics

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster.png

512

1024

Serena Hajjar

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Serena Hajjar2021-03-15 05:31:572021-03-15 05:31:57Public vs. Private Employment in Massachusetts: A Tale of Two Pandemics https://pioneerinstitute.org/wp-content/uploads/Yellow-and-Green-2-Circle-Venn-Diagram-1.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-03-10 05:39:542021-03-10 05:39:54Lessons for Massachusetts from California’s “blank check” tax on high earners

https://pioneerinstitute.org/wp-content/uploads/Yellow-and-Green-2-Circle-Venn-Diagram-1.png

512

1024

Greg Sullivan

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Greg Sullivan2021-03-10 05:39:542021-03-10 05:39:54Lessons for Massachusetts from California’s “blank check” tax on high earners https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Kevin Martin

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Kevin Martin2021-03-02 05:51:302021-03-02 05:58:09The Graduated Income Tax Amendment – A Shell Game?

https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Kevin Martin

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Kevin Martin2021-03-02 05:51:302021-03-02 05:58:09The Graduated Income Tax Amendment – A Shell Game? https://pioneerinstitute.org/wp-content/uploads/CA-report.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-02-22 05:06:222021-03-22 14:01:49How a 2012 income tax hike cost California billions of dollars in economic activity

https://pioneerinstitute.org/wp-content/uploads/CA-report.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-02-22 05:06:222021-03-22 14:01:49How a 2012 income tax hike cost California billions of dollars in economic activity https://pioneerinstitute.org/wp-content/uploads/Hubwonk-Template-4.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-02-10 05:25:522021-03-22 13:57:40Barriers to Exit Lowered in High-Cost States as Pandemic-Related Technologies Changed Outlook

https://pioneerinstitute.org/wp-content/uploads/Hubwonk-Template-4.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-02-10 05:25:522021-03-22 13:57:40Barriers to Exit Lowered in High-Cost States as Pandemic-Related Technologies Changed Outlook