The Myth of Cost Control Legislation

The House passed their version of “cost control” last night in a 148-7 vote. Sadly for taxpayers and the general public, there was little debate on the bill itself and the few minutes of debate on the floor revolved exclusively around a handful of amendments. Changing 18% of our state economy with little debate, no hard questions, in a few hours, no problem? Was this how we did it for health reform 1.0?

The leadership accepted most special interest amendments in an effort to garner votes. Most of these provisions will be taken out in conference committee.

What We Know

- 18% of the Massachusetts economy is health care related;

- 20% of patients account for 80% of costs, 5% of patients account for 50% of costs;

- 70% of health care costs are lifestyle related,

- 74% of costs fall into: cardiovascular disease, cancer, diabetes & obesity.

- Legislature regulates less than 40% of residents’ health insurance.

5 Reasons Why Mass. Payment Reform Bills Won’t Work

This is not a health care cost containment bill. It may (open question) result in better care, but its changes do not correlate with less expensive care. The bill won’t save money on a net basis and won’t save $10B (ave.) every year for 15 years, as being promised.

Surcharges will add $100s MMs to the system. Spending new money may be a wise investment in some cases, but the Legislature must be honest about the added costs. And when will the savings materialize? 2014, 2017, 2037?

- The bill is built on unrealistic savings estimates.

Massachusetts spends ~$70 B/yr on health care. The House goal is to cut, on average, $10 B/yr over 15 years. But State will only impact 40% of market. That 40% spends roughly $13B/yr. Does the House really intend on almost zeroing out the spending of the 40% they regulate for 15 straight years?

One is left to wonder what will be cut: hospitals, access to care, waste, wages and jobs.

Note: *This is an underestimate of covered lives in self-insured arrangements: It uses as a proxy DHCFP data showing 53% of companies report being self-insured, and ignores the number of covered lives for their employees and their family members; that is, the state can impact even fewer lives then in this analysis. ** House bill seeks a Federal waiver to run the Medicare population, a significant change from the status quo. ***Different methods for collecting data from the different sources account for the overestimate of population. Mass. has 6.5MM residents. In addition, but not included in these numbers are the 30% of covered lives in the commercial market already on an alternative payment contract. Do we expect significant additional savings from this group?

2. The bill trusts bureaucrats to lead the health care market.

The bill gives state employees authority (and assumes their expertise) to determine 18% of our state’s economy; specifically, to:

- Determine financial solvency, collaboration requirements, and track market-share interactions for/between ACOs.

- Set the intricacies of payment contracts and how much risk health care professions can take. Set the right amount of reimbursement in a global/ bundled payment to sustain medical research.

- Decide (via effective bureaucracy?) who gets to build what, where, why, when (Determination of Need)

- Determine the future of medicine, with controls over medical innovation.

- Know when to act or not act. Tremendous latitude given to the division to take “appropriate actions,” or establish when something is “deemed to be excessive.” Approve contracts only when a “sufficient amount” of a current action is present. This is ripe for political influence and future lawsuits, adding cost.

3. Most importantly, it sidesteps the only long-term sustainable solution to health care cost increases, meaningful engagement of consumers.

- Bill takes some half steps in the right direction on transparency, but open question if the information provided will be helpful to patients. If insurance design does not incentivize the low-cost high-quality provider, then many patients will pick the high-cost provider (the opposite outcome the Legislature wants).

- Health Affairs study found that expanding the use of patient-centered health plans from their current share of 13% of the employer-sponsored marketplace to 50% would reduce health costs by $57 billion per year. 100% uptake would result in over $100 B in savings a year.[1]

- Imagine the savings in Massachusetts as patient-centered health plans make up only 3% of covered lives, much lower than the national average of 13%.

- Patients need to be active agents in their own health, and be rewarded for healthy behavior. The research shows the best and most effective method is patient-centered (consumer-directed) health plans, many include a HSA (health savings account) and/or a HRA (health reimbursement account).

- Whole Foods and others like Safeway have led the way in patient-centered health plans.[2]

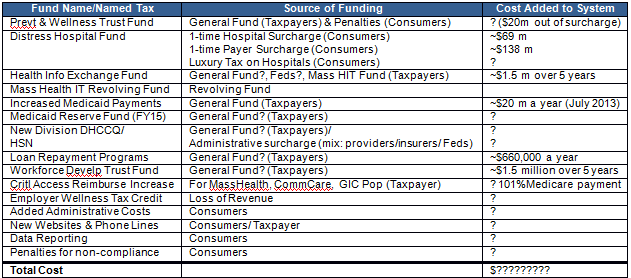

4. It adds significant costs to the health care system, directly and indirectly.

[1] http://bit.ly/KFYJHv

[2] http://on.wsj.com/KaTEoh, http://on.wsj.com/KG89Ts

5. It puts tremendous faith in unproven ACOs, alternative payment methodologies, and HIT.

ACOs

- Medicare ran ACO-pilot (Physicians’ Group Practice, 2005-10) with nation’s most respected group practices. The results were disappointing. Only two groups achieved 1st-year savings; only ½ of groups did after 3 yrs, but not every year.[3]

- Some claim ACOs are different from HMOs, but they operate on same risk principle and use some form of capitated payments. Capitated payments are not intrinsically bad, but consumers must buy-in. The contracts place most of the burden on providers to change a patient’s behavior and hold the risk if they fail.

- 2012 Mass. Medical Society survey found only 29% of doctors reported that “their group is ready to enter global payment contracts.” Only 44% believe global payments will decrease spending. Only 19% believe they will improve quality. 76% said global payments would reduce the number of physicians willing to work in Mass.[4]

- In ACOs, providers are accountable to the payer. Patients won’t get savings if care is delivered well/less expensively.

- ACOs drive more power to hospitals.

- Estimated start-up costs are $10-30 m for a midsize market system without managed care experience.

Alternative Payments

- Fee-for-service payments can result in perverse incentives to provide more care.

- Attorney General’s report found that providers paid by global payment care have tended to end up costing more, and did not correlate with higher quality care.[5]

- Switching payment method does not fix the issue. Bundled payments can result in perverse incentives to provide more care, providing more bundles. Global capitated payments can result in a perverse incentive to withhold care.

- The one way to end the incentive dilemma is to allow consumers to pick with flexible insurance plan design.

HIT

- Numerous reports have documented the risk and reward of health IT systems, in some cases they have added cost after full implementation.[6]

Find me on twitter: @josharchambault

[1] http://bit.ly/KFYJHv

[2] http://on.wsj.com/KaTEoh, http://on.wsj.com/KG89Ts

[3] NEJM- “Lessons from the PGP Demonstration – A Sobering Reflection,” http://bit.ly/M0ErFK, WSJ – http://on.wsj.com/NoYeBk, A former Obama adviser found the same mixed results in [NEJM “ACO- A 3yr Financial Loss?” http://bit.ly/L8TwJD

[4] http://bit.ly/JH5lS7

[5] http://1.usa.gov/M0HE8d

[6] Health Affairs- http://bit.ly/Lgd274, NCPA- http://bit.ly/Lt8tT7