Jon Gruber’s RomneyCare/ObamaCare False Narrative

This morning, Steve LeBlanc of the Associated Press has another Massachusetts focused story up titled “Mass. Health Law May Bode Well for Federal Law.”

The piece is based on a common flawed assumption. The piece fails to mention Massachusetts’ pre-reform circumstances in contrast to other states now. It expects that the same actions and behaviors will play out in the same way in other states.

To expand on my quote in the story, can we honestly suppose New Mexico with 20+% uninsured, no guarantee issue in their individual market, employer sponsored insurance rates of 48.6 percent, lower income levels, lower education level, low-medical infrastructure, and a geographically spread out state to see the exact same results as the Commonwealth?

Contrast that with the starting place in the Commonwealth and it looks like two different planets.

MIT professor Jonathan Gruber is out there selling the “expect the same” narrative to the media for the national healthcare law, but that is not what his consulting reports are saying for states. One only has to review his reports to Wisconsin, Minnesota, and Colorado for examples of the disruption that even he predicts. Avik Roy at Forbes.com wrote on the topic in March:

Gruber now: Obamacare will increase premiums by 19-30 percent

As states began the process of considering whether or not to set up the insurance exchanges mandated by the new health law, several retained Gruber as a consultant. In at least three cases—Wisconsin in August 2011, Minnesota in November 2011, andColorado in January 2012—Gruber reported that premiums in the individual market would increase, not decrease, as a result of Obamacare.

In Wisconsin, Gruber reported that people purchasing insurance for themselves on the individual market would see, on average, premium increases of 30 percent by 2016, relative to what would have happened in the absence of Obamacare. In Minnesota, the law would increase premiums by 29 percent over the same period. Colorado was the least worst off, with premiums under the law rising by only 19 percent.

Some low-income individuals would benefit from Obamacare’s subsidies; for those individuals, the impact of these premium increases would be blunted. But if premium costs go up at a rate faster than people expect, taxpayers will be on the hook for billions upon billions of extra subsidies.

UPDATE: Gruber objects to the characterization of his state reports since some individuals will also receive a tax credit. However his argument holds little water since a tax credit is only taking money out of your right hand and handing it back to your left hand in the form of a credit for more expensive insurance.

Finally, after reading the AP story, a few cautionary notes on data points is needed:

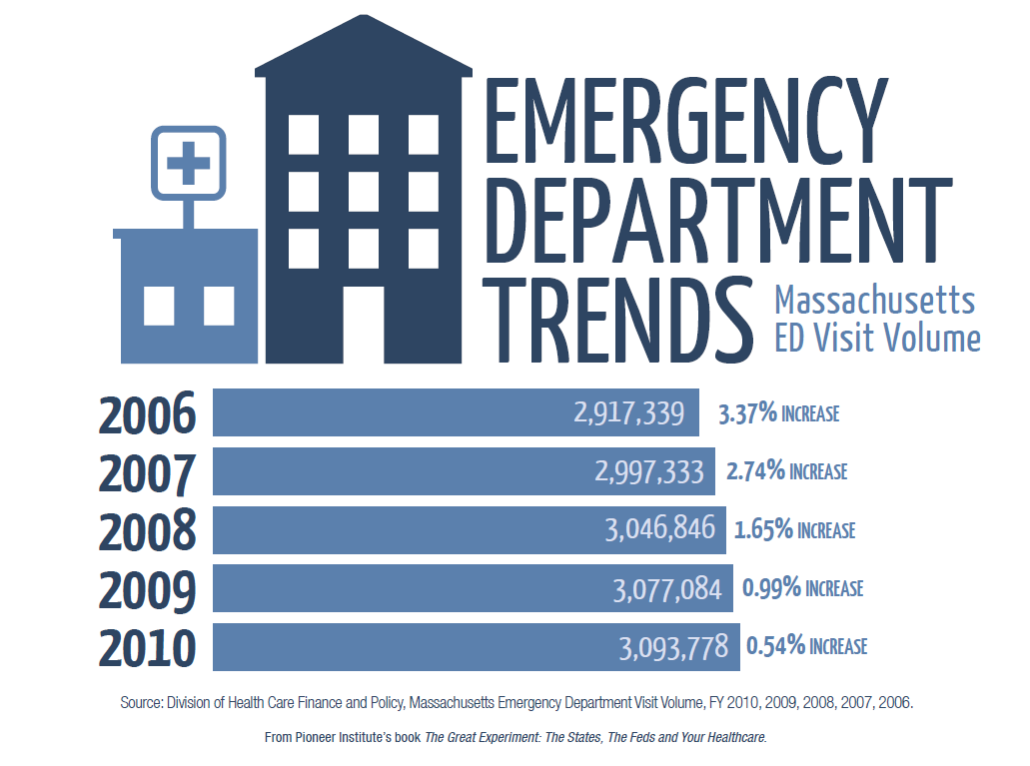

1. ER data decrease. I believe only one BCBS Foundation report found a self-reported decrease in visits. From a research standpoint, especially with a down economy and less people seeking out medical care, this is not enough to say visits are going down. We can hope so, but further data is needed before we can say this is a trend, as we have seen six years of increases.

2. In the article it is written,

Another indication of the law’s acceptance in Massachusetts is the reduction in the number of those assessed a tax penalty for failing to have insurance despite being able to afford it. In 2010, 44,000 Massachusetts tax filers were assessed the penalty under the “individual mandate.” That’s a drop from the 67,000 people required to pay the penalty in 2007, the first year it was assessed.

I blogged on the data yesterday. Are Fewer People in MA Paying the Indiv Mandate Penalty? What you find is that more than 50,000 additional people have received an exemption from 2008-2010; I would say that calls into question the greater acceptance explanation.

3. As far as the MTF report is concerned on cost that is mentioned in the article, language is really important here. The MTF language from their report on the cost of the 2006 reform is, “the incremental additional state cost per year has averaged $91 million…”

This is a very strange way to interpret the cost data. A better number to highlight would be the incremental increase each year over the 2006 baseline (i.e. if we didn’t have reform).

I blogged on this issue as well recently explaining how to breakdown the cost data. Is Romneycare A Budget Buster? What we find is that compared to what we were spending in 2006 on average we are paying $738 million more with the state share being about $369 million per year. That is a much different story than the $91 million being widely reported. The blog goes into greater detail for those that are interested.

Find me on twitter: @josharchambault