Fair Share Amendment: Weighing Costs & Benefits for Massachusetts’ Economy & Workers

Hubwonk host Joe Selvaggi talks with Pioneer Institute’s Executive Director Jim Stergios about HB86, the so-called Fair Share Amendment, to tax Massachusetts household income above $1 million. They discuss its promises, its costs, and the effects of similar legislation in other states.

Learn about Pioneer Institute’s research on the economic impact of tax policy.

Guest:

Jim Stergios is Executive Director of Pioneer Institute, a Boston-based think tank founded in 1988. Prior to joining Pioneer, Jim was Chief of Staff and Undersecretary for Policy in Massachusetts’ Executive Office of Environmental Affairs, where he drove efforts on water policy, regulatory and permit reform, and urban revitalization. His prior experience includes founding and managing a business, teaching at the university level, and serving as headmaster at a preparatory school. Jim serves on the Board of Advisors at Boston University, where he earned a doctoral degree in Political Science. Jim has been interviewed on numerous news outlets and appears regularly on local television and radio broadcasts, including WBZ, WHDH, WCVB, NECN, Boston 25, WGBH, WBUR, Nightside with Dan Rea, and WRKO. Jim’s opinion pieces have appeared in The Wall Street Journal, The Hill, The Boston Globe, and regional newspapers throughout New England.

Jim Stergios is Executive Director of Pioneer Institute, a Boston-based think tank founded in 1988. Prior to joining Pioneer, Jim was Chief of Staff and Undersecretary for Policy in Massachusetts’ Executive Office of Environmental Affairs, where he drove efforts on water policy, regulatory and permit reform, and urban revitalization. His prior experience includes founding and managing a business, teaching at the university level, and serving as headmaster at a preparatory school. Jim serves on the Board of Advisors at Boston University, where he earned a doctoral degree in Political Science. Jim has been interviewed on numerous news outlets and appears regularly on local television and radio broadcasts, including WBZ, WHDH, WCVB, NECN, Boston 25, WGBH, WBUR, Nightside with Dan Rea, and WRKO. Jim’s opinion pieces have appeared in The Wall Street Journal, The Hill, The Boston Globe, and regional newspapers throughout New England.

Get new episodes of Hubwonk in your inbox!

Related Posts

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-09 09:29:102021-06-09 09:29:10This Is No Time for a Tax Increase

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-10.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-09 09:29:102021-06-09 09:29:10This Is No Time for a Tax Increase https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-01 05:54:112021-06-01 05:54:11Study Finds Deep Flaws in Advocates’ Claims that the Massachusetts Tax Code is Regressive

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-06-01 05:54:112021-06-01 05:54:11Study Finds Deep Flaws in Advocates’ Claims that the Massachusetts Tax Code is Regressive https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-05-05 05:33:362021-05-05 06:04:38Study Says Interstate Tax Competition, Relocation Subsidies Exacerbate Telecommuting Trends

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-7.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-05-05 05:33:362021-05-05 06:04:38Study Says Interstate Tax Competition, Relocation Subsidies Exacerbate Telecommuting Trends https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-26 05:08:592021-04-26 05:22:50Study Warns Massachusetts Tax Proposal Would Deter Investment, Stifling the “Innovation Economy”

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CG8.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-26 05:08:592021-04-26 05:22:50Study Warns Massachusetts Tax Proposal Would Deter Investment, Stifling the “Innovation Economy” https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-20 05:46:542021-04-20 15:51:32Study Shows the Adverse Effects of Graduated Income Tax Proposal on Small Businesses

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-4.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-20 05:46:542021-04-20 15:51:32Study Shows the Adverse Effects of Graduated Income Tax Proposal on Small Businesses https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-07 05:47:152021-04-07 05:47:15Study: Graduated Income Tax Proposal Fails to Protect Taxpayers from Bracket Creep

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-07 05:47:152021-04-07 05:47:15Study: Graduated Income Tax Proposal Fails to Protect Taxpayers from Bracket Creep https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-01 05:56:422021-04-01 07:11:11New Study Warns Graduated Income Tax Will Harm Many Massachusetts Retirees

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-04-01 05:56:422021-04-01 07:11:11New Study Warns Graduated Income Tax Will Harm Many Massachusetts Retirees https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-25 05:46:072021-04-01 06:00:36Study: Graduated Income Tax Proponents Rely on Analyses That Exclude the Vast Majority Of “Millionaires” to Argue Their Case

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-25 05:46:072021-04-01 06:00:36Study: Graduated Income Tax Proponents Rely on Analyses That Exclude the Vast Majority Of “Millionaires” to Argue Their Case https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-15 05:43:412021-03-15 05:45:37Report Contrasts State Government and Private Sector Employment Changes During Pandemic

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-15 05:43:412021-03-15 05:45:37Report Contrasts State Government and Private Sector Employment Changes During Pandemic https://pioneerinstitute.org/wp-content/uploads/Yellow-and-Green-2-Circle-Venn-Diagram-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-10 05:41:292021-03-10 06:28:08Study Finds Massachusetts Graduated Income Tax May Be a “Blank Check” and Not Increase Funding for Designated Priorities

https://pioneerinstitute.org/wp-content/uploads/Yellow-and-Green-2-Circle-Venn-Diagram-1.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-10 05:41:292021-03-10 06:28:08Study Finds Massachusetts Graduated Income Tax May Be a “Blank Check” and Not Increase Funding for Designated Priorities https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-02 05:55:462021-03-02 06:36:19Report: Proposed Graduated Income Tax Might Not Increase State Education and Transportation Spending

https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-02 05:55:462021-03-02 06:36:19Report: Proposed Graduated Income Tax Might Not Increase State Education and Transportation Spending https://pioneerinstitute.org/wp-content/uploads/Fig1-5.png

601

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

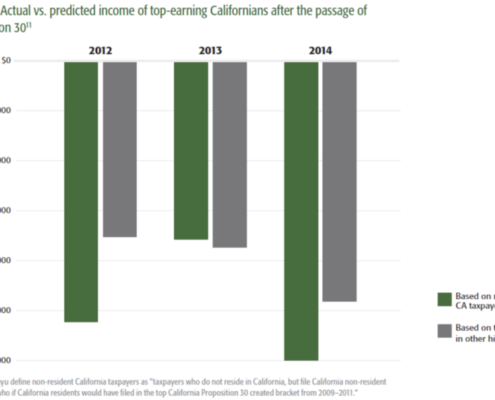

Editorial Staff2021-02-22 05:18:182021-02-22 06:08:55New Study Highlights Economic Fallout from California’s 2012 Tax Hike

https://pioneerinstitute.org/wp-content/uploads/Fig1-5.png

601

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-02-22 05:18:182021-02-22 06:08:55New Study Highlights Economic Fallout from California’s 2012 Tax Hike