Tag Archive for: graduated income tax

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-25 05:46:072021-04-01 06:00:36Study: Graduated Income Tax Proponents Rely on Analyses That Exclude the Vast Majority Of “Millionaires” to Argue Their Case

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-25 05:46:072021-04-01 06:00:36Study: Graduated Income Tax Proponents Rely on Analyses That Exclude the Vast Majority Of “Millionaires” to Argue Their Case https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-03-25 05:34:372021-12-29 12:19:26Missing the Mark on Wealth Migration: Past Studies Drastically Undercounted Millionaires

https://pioneerinstitute.org/wp-content/uploads/Copy-of-CY3-1.png

512

1024

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2021-03-25 05:34:372021-12-29 12:19:26Missing the Mark on Wealth Migration: Past Studies Drastically Undercounted Millionaires https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-15 05:43:412021-03-15 05:45:37Report Contrasts State Government and Private Sector Employment Changes During Pandemic

https://pioneerinstitute.org/wp-content/uploads/Red-and-Dark-Sienna-Music-Poster.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-15 05:43:412021-03-15 05:45:37Report Contrasts State Government and Private Sector Employment Changes During Pandemic https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-02 05:55:462021-03-02 06:36:19Report: Proposed Graduated Income Tax Might Not Increase State Education and Transportation Spending

https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Kevin Martin

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Kevin Martin2021-03-02 05:51:302021-03-02 05:58:09The Graduated Income Tax Amendment – A Shell Game?

https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-03-02 05:55:462021-03-02 06:36:19Report: Proposed Graduated Income Tax Might Not Increase State Education and Transportation Spending

https://pioneerinstitute.org/wp-content/uploads/CA-report-2.png

512

1024

Kevin Martin

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Kevin Martin2021-03-02 05:51:302021-03-02 05:58:09The Graduated Income Tax Amendment – A Shell Game? https://pioneerinstitute.org/wp-content/uploads/Fig1-3.png

652

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

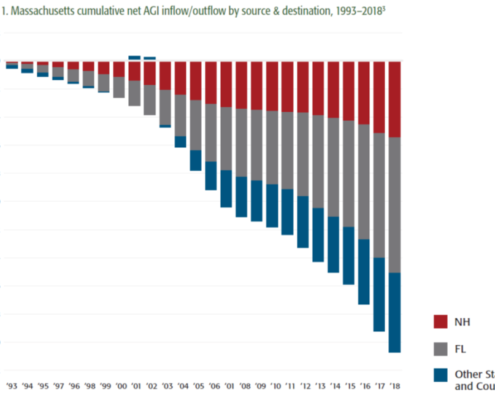

Editorial Staff2021-02-01 05:10:572021-07-22 09:09:56New Study Shows Significant Wealth Migration from Massachusetts to Florida, New Hampshire

https://pioneerinstitute.org/wp-content/uploads/Fig1-3.png

652

923

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2021-02-01 05:10:572021-07-22 09:09:56New Study Shows Significant Wealth Migration from Massachusetts to Florida, New Hampshire