https://pioneerinstitute.org/wp-content/uploads/Screenshot-2024-07-26-101538.png

480

724

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-07-26 10:19:532024-07-26 10:19:53Massachusetts Affordability and Competitiveness Ranking is in Freefall

https://pioneerinstitute.org/wp-content/uploads/Screenshot-2024-07-26-101538.png

480

724

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-07-26 10:19:532024-07-26 10:19:53Massachusetts Affordability and Competitiveness Ranking is in Freefall https://pioneerinstitute.org/wp-content/uploads/lazaro-rodriguez-Ij5oHzQEh8Q-unsplash.jpg

2237

2237

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-17 17:33:452024-07-17 17:33:31Study: U.S. Immigration System Limits Benefits Foreign Students Could Provide

https://pioneerinstitute.org/wp-content/uploads/lazaro-rodriguez-Ij5oHzQEh8Q-unsplash.jpg

2237

2237

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-17 17:33:452024-07-17 17:33:31Study: U.S. Immigration System Limits Benefits Foreign Students Could Provide https://pioneerinstitute.org/wp-content/uploads/1806_Massachusetts_Bay_Community_College_DWA_HE_MBCC_Academic_1.5f14066753d98da41ba696d919b5ec55.jpg

381

831

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-07-10 14:10:162024-07-10 21:00:36Is Free Community College What Massachusetts Needs?

https://pioneerinstitute.org/wp-content/uploads/1806_Massachusetts_Bay_Community_College_DWA_HE_MBCC_Academic_1.5f14066753d98da41ba696d919b5ec55.jpg

381

831

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-07-10 14:10:162024-07-10 21:00:36Is Free Community College What Massachusetts Needs? https://pioneerinstitute.org/wp-content/uploads/IRS-Statement-3.png

464

718

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-01 15:51:162024-07-01 15:51:16Latest IRS Migration Data Show Exodus from Massachusetts Continues

https://pioneerinstitute.org/wp-content/uploads/IRS-Statement-3.png

464

718

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-07-01 15:51:162024-07-01 15:51:16Latest IRS Migration Data Show Exodus from Massachusetts Continues https://pioneerinstitute.org/wp-content/uploads/Monthly-Musings-June.png

475

717

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-06-13 10:45:452024-06-13 10:45:45Massachusetts Legislature Procrastinates Once Again

https://pioneerinstitute.org/wp-content/uploads/Monthly-Musings-June.png

475

717

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-06-13 10:45:452024-06-13 10:45:45Massachusetts Legislature Procrastinates Once Again https://pioneerinstitute.org/wp-content/uploads/immigrant-entrepreneurship.png

473

703

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-13 00:00:362024-06-12 14:56:18Study Finds Prevalence of Entrepreneurship Tied to Regulatory Environment, Portion of Immigrants

https://pioneerinstitute.org/wp-content/uploads/immigrant-entrepreneurship.png

473

703

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-06-13 00:00:362024-06-12 14:56:18Study Finds Prevalence of Entrepreneurship Tied to Regulatory Environment, Portion of Immigrants https://pioneerinstitute.org/wp-content/uploads/FY25-Budget-Blog-05092024.png

460

700

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-05-09 13:11:182024-05-09 13:11:18Commentary On The Senate Ways And Means Committee FY2025 Budget

https://pioneerinstitute.org/wp-content/uploads/FY25-Budget-Blog-05092024.png

460

700

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-05-09 13:11:182024-05-09 13:11:18Commentary On The Senate Ways And Means Committee FY2025 Budget  https://pioneerinstitute.org/wp-content/uploads/Blog-McAnneny-Milton-housing-02152024.png

1400

1400

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-02-15 14:55:462024-02-15 14:55:46Milton Shuts the Door

https://pioneerinstitute.org/wp-content/uploads/Blog-McAnneny-Milton-housing-02152024.png

1400

1400

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-02-15 14:55:462024-02-15 14:55:46Milton Shuts the Dooron Multifamily Housing Plans

https://pioneerinstitute.org/wp-content/uploads/Mass-Reveneue-Decline-013120242.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-02-06 11:15:152024-02-06 14:06:31Pioneer Statement on Continuing Slide in Massachusetts’ Revenue

https://pioneerinstitute.org/wp-content/uploads/Mass-Reveneue-Decline-013120242.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-02-06 11:15:152024-02-06 14:06:31Pioneer Statement on Continuing Slide in Massachusetts’ Revenue https://pioneerinstitute.org/wp-content/uploads/Mass-Reveneue-Decline-01312024.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-01-31 13:45:522024-01-31 13:24:26Pioneer Statement on Decline in State Revenues

https://pioneerinstitute.org/wp-content/uploads/Mass-Reveneue-Decline-01312024.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2024-01-31 13:45:522024-01-31 13:24:26Pioneer Statement on Decline in State Revenues https://pioneerinstitute.org/wp-content/uploads/Op-ed-Schedule-A-Enright-01292024.png

1400

1400

Aidan Enright

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Aidan Enright2024-01-29 15:39:002024-01-29 15:39:00Skill-based immigration could ease labor shortage

https://pioneerinstitute.org/wp-content/uploads/Op-ed-Schedule-A-Enright-01292024.png

1400

1400

Aidan Enright

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Aidan Enright2024-01-29 15:39:002024-01-29 15:39:00Skill-based immigration could ease labor shortage https://pioneerinstitute.org/wp-content/uploads/Blog-Budget-McAnneny-011120242.png

1400

1400

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-01-11 15:03:092024-01-11 15:03:09My Musings on Massachusetts’ Fiscal Picture

https://pioneerinstitute.org/wp-content/uploads/Blog-Budget-McAnneny-011120242.png

1400

1400

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2024-01-11 15:03:092024-01-11 15:03:09My Musings on Massachusetts’ Fiscal Picture https://pioneerinstitute.org/wp-content/uploads/Workforce-Development-120420232.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-12-04 09:25:252023-12-04 07:21:32The Massachusetts Workforce: Abundant Resources, Steep Challenges

https://pioneerinstitute.org/wp-content/uploads/Workforce-Development-120420232.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-12-04 09:25:252023-12-04 07:21:32The Massachusetts Workforce: Abundant Resources, Steep Challenges https://pioneerinstitute.org/wp-content/uploads/Benefit-Cliffs-Paper-11062023.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-11-06 09:00:562023-11-03 16:06:46New Report Explores Impact of Welfare Benefit Cliffs

https://pioneerinstitute.org/wp-content/uploads/Benefit-Cliffs-Paper-11062023.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-11-06 09:00:562023-11-03 16:06:46New Report Explores Impact of Welfare Benefit Cliffs https://pioneerinstitute.org/wp-content/uploads/Tax-Relief-09292023.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-09-29 11:01:542023-09-29 12:46:33Pioneer Institute Statement on the State Legislature’s FY2024 Tax Relief Package

https://pioneerinstitute.org/wp-content/uploads/Tax-Relief-09292023.png

1400

1400

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-09-29 11:01:542023-09-29 12:46:33Pioneer Institute Statement on the State Legislature’s FY2024 Tax Relief Package https://pioneerinstitute.org/wp-content/uploads/Senate-Bill-analysis-06142023.png

1080

2400

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2023-06-14 06:30:412023-06-14 06:40:44Senate Tax Package Misses the Mark on Competitiveness

https://pioneerinstitute.org/wp-content/uploads/Senate-Bill-analysis-06142023.png

1080

2400

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2023-06-14 06:30:412023-06-14 06:40:44Senate Tax Package Misses the Mark on Competitiveness https://pioneerinstitute.org/wp-content/uploads/Immigrant-Entre-image.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-06-08 09:01:272023-06-01 15:23:35Study: Immigrant Entrepreneurs Benefit N.E. Economy, Despite Facing Obstacles to Growth

https://pioneerinstitute.org/wp-content/uploads/Immigrant-Entre-image.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-06-08 09:01:272023-06-01 15:23:35Study: Immigrant Entrepreneurs Benefit N.E. Economy, Despite Facing Obstacles to Growth https://pioneerinstitute.org/wp-content/uploads/Screenshot-2023-05-12-at-5.42.35-PM.png

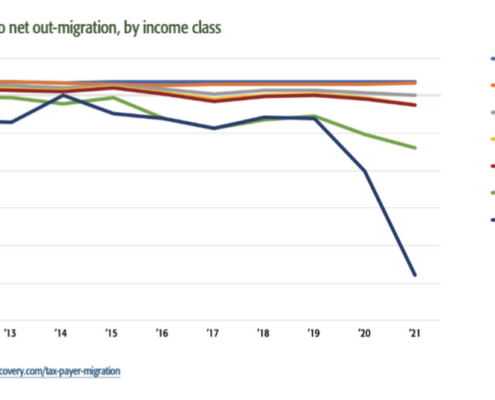

535

1042

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-05-15 09:00:492023-06-22 13:17:57Study: Net Out-Migration of Wealth from Massachusetts Nearly Quintupled from 2012-2021

https://pioneerinstitute.org/wp-content/uploads/Screenshot-2023-05-12-at-5.42.35-PM.png

535

1042

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-05-15 09:00:492023-06-22 13:17:57Study: Net Out-Migration of Wealth from Massachusetts Nearly Quintupled from 2012-2021 https://pioneerinstitute.org/wp-content/uploads/work-force.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-05-02 09:11:232023-05-03 15:37:07Study Finds Massachusetts Workforce Has Become More Female, Older, More Diverse

https://pioneerinstitute.org/wp-content/uploads/work-force.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-05-02 09:11:232023-05-03 15:37:07Study Finds Massachusetts Workforce Has Become More Female, Older, More Diverse https://pioneerinstitute.org/wp-content/uploads/Statement-on-tax-reform-and-budget.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-19 09:00:272023-04-19 09:27:17Public Statement on the House’s Proposed Tax Reform and Budget

https://pioneerinstitute.org/wp-content/uploads/Statement-on-tax-reform-and-budget.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-19 09:00:272023-04-19 09:27:17Public Statement on the House’s Proposed Tax Reform and Budget https://pioneerinstitute.org/wp-content/uploads/Tax-Migration-4-Enright.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-14 09:05:392023-05-02 11:27:05Debunking Migration Myths, Part 2

https://pioneerinstitute.org/wp-content/uploads/Tax-Migration-4-Enright.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-14 09:05:392023-05-02 11:27:05Debunking Migration Myths, Part 2 https://pioneerinstitute.org/wp-content/uploads/Tax-Migration-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-11 08:45:022023-04-10 17:47:18Debunking Tax Migration Myths

https://pioneerinstitute.org/wp-content/uploads/Tax-Migration-3.png

512

1024

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2023-04-11 08:45:022023-04-10 17:47:18Debunking Tax Migration Myths https://pioneerinstitute.org/wp-content/uploads/Tax-Analysis.png

512

1024

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2023-03-03 10:50:382023-03-10 11:07:03Gov. Healey’s Tax Plan: Not Enough on Competitiveness

https://pioneerinstitute.org/wp-content/uploads/Tax-Analysis.png

512

1024

Eileen McAnneny

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Eileen McAnneny2023-03-03 10:50:382023-03-10 11:07:03Gov. Healey’s Tax Plan: Not Enough on Competitiveness https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-13.png

512

1024

Josh Bedi

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Josh Bedi2022-12-08 08:13:062022-12-08 08:13:15Immigrant Entrepreneurs and the Barriers They Face: An Academic Literature Review

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-13.png

512

1024

Josh Bedi

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Josh Bedi2022-12-08 08:13:062022-12-08 08:13:15Immigrant Entrepreneurs and the Barriers They Face: An Academic Literature Review https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-10.png

512

1024

Tom Ahn

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Tom Ahn2022-09-21 10:11:192022-09-21 10:11:19What We Do and Don’t Know about Online Platform Rideshare/Delivery Workers in Massachusetts

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-10.png

512

1024

Tom Ahn

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Tom Ahn2022-09-21 10:11:192022-09-21 10:11:19What We Do and Don’t Know about Online Platform Rideshare/Delivery Workers in Massachusetts https://pioneerinstitute.org/wp-content/uploads/Untitled-design-2022-05-25T083008.246.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-05-25 08:30:492022-07-06 07:51:30Book Reveals How Tax Hike Amendment Would Damage Commonwealth’s Economic Competitiveness

https://pioneerinstitute.org/wp-content/uploads/Untitled-design-2022-05-25T083008.246.png

512

1000

Editorial Staff

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Editorial Staff2022-05-25 08:30:492022-07-06 07:51:30Book Reveals How Tax Hike Amendment Would Damage Commonwealth’s Economic Competitiveness https://pioneerinstitute.org/wp-content/uploads/public-statement-3.png

900

1600

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2022-05-18 21:31:002022-05-18 21:31:00The MBTA’s Automated Fare Collection Modernization Contract: Over-Budget And Behind Schedule, But Now Back On Track

https://pioneerinstitute.org/wp-content/uploads/public-statement-3.png

900

1600

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2022-05-18 21:31:002022-05-18 21:31:00The MBTA’s Automated Fare Collection Modernization Contract: Over-Budget And Behind Schedule, But Now Back On Track https://pioneerinstitute.org/wp-content/uploads/public-statement-zoning.png

900

1600

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2022-04-11 10:03:442022-04-11 10:03:44A Vision for Sustainable, Transit-oriented Development

https://pioneerinstitute.org/wp-content/uploads/public-statement-zoning.png

900

1600

Andrew Mikula

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Andrew Mikula2022-04-11 10:03:442022-04-11 10:03:44A Vision for Sustainable, Transit-oriented Development https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-2.png

512

1024

Collin Quigley

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Collin Quigley2022-02-08 06:06:582022-02-08 06:06:58Bus Rapid Transit: Costs and Benefits of a Transit Alternative

https://pioneerinstitute.org/wp-content/uploads/Copy-of-11.-Employees-of-the-Public-Sector-1-2.png

512

1024

Collin Quigley

https://pioneerinstitute.org/wp-content/uploads/logo_440x96.png

Collin Quigley2022-02-08 06:06:582022-02-08 06:06:58Bus Rapid Transit: Costs and Benefits of a Transit Alternative