August 10, 2026

New Study Finds Massachusetts Is Not Progressive When It Comes to Taxing Lower- and Middle-Income Families

Commonwealth taxes a larger share of typical families’ income than competing states, relying on a patchwork of credits instead of broad relief

BOSTON – On the heels of last week’s unprecedented state Supreme Judicial Court (SJC) decision removing a widely supported income-tax reduction measure from the November ballot, a new Pioneer Institute study finds that Massachusetts taxes a far larger share of lower- and middle-income households’ earnings compared to red and blue competitor states.

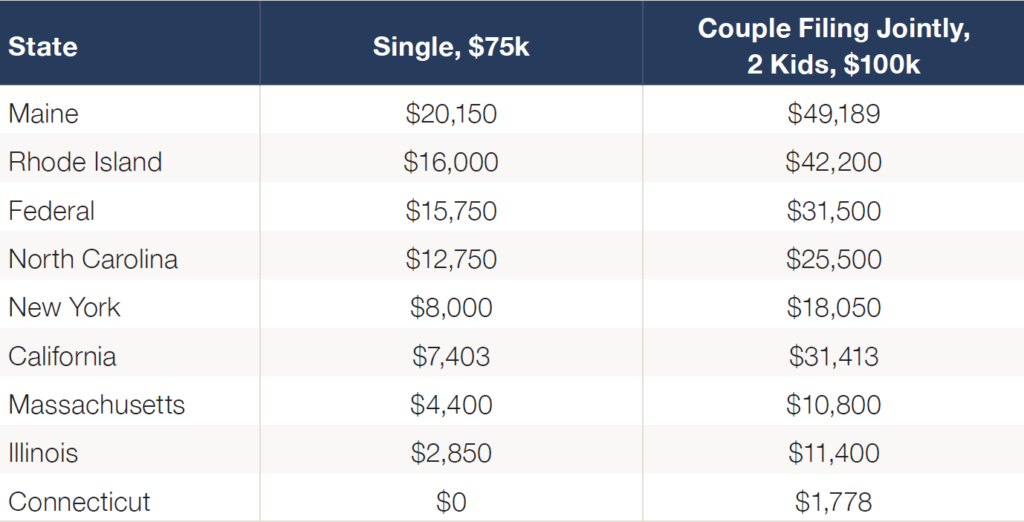

The Commonwealth’s personal exemption remains at just $4,400 for single filers and $8,800 for married couples filing jointly—levels that have not changed since 2008 and have declined in inflation-adjusted value by 55 percent. If rates had been adjusted for inflation, they would have saved tax filers an additional $861 million in 2025. Current rates shield far less income from Massachusetts taxpayers than many competing and neighboring states.

By comparison, North Carolina shields $12,750 for single filers and $25,500 for married couples, while the federal standard deduction shields $15,750 and $31,500, respectively. Neighboring states also provide more generous protection from taxation: Maine allows single filers to deduct up to the equivalent of $20,150, while Rhode Island shields $16,000.

“States like North Carolina shield nearly three times as much income from taxation as Massachusetts does,“ said Aidan Enright, co-author of Universal or Targeted? Is Massachusetts an Outlier in How It Delivers Tax Relief to Lower- and Middle-Income Households? “Massachusetts prides itself in supporting lower income populations, but many states provide considerably more broad-based tax relief to lower- and middle-income families.”

As a result, Massachusetts begins taxing ordinary households at significantly lower income levels than many of the states with which it competes.

A married couple earning $100,000 pays taxes on $91,200 of income in Massachusetts before additional eligibility-based credits and deductions are applied, compared with just $74,500 in North Carolina. At Massachusetts’ 5 percent income tax rate, that difference leaves Massachusetts couples paying $835 more in taxes. When North Carolina’s lower income tax rate of 3.99 percent is taken into account, the difference approaches $1,400 annually.

Figure 1: Comparison of Combined Base Standard Deductions and Personal Exemptions for Select States, 2025

The findings come days after the SJC blocked a ballot initiative to reduce the state’s income tax rate from 5 to 4 percent. Polling consistently showed the measure was headed for approval, but the court invalidated it because of a drafting error by a government office, not by the measure’s supporters or the hundreds of thousands of Massachusetts residents who signed petitions to place it on the ballot.

“The court has established a dangerous precedent by disenfranchising voters because of a mistake made by a government official,” said Jim Stergios, executive director of Pioneer Institute. “But while the court may have removed the question from the ballot, it did not remove the underlying problem. Massachusetts continues to impose a heavy burden on all taxpayers, including lower- and middle-income families struggling with some of the nation’s highest housing, healthcare and energy costs.”

Unlike many states that rely on broad standard deductions, Massachusetts is heavily dependent on a collection of targeted credits and deductions, including those for children, renters, seniors, commuters, and student-loan borrowers. These provisions provide important relief, but because they are not universal, they require taxpayers to navigate complex eligibility and filing requirements.

“Massachusetts politicians speak the language of progressivism, but our tax code tells a different story,” Stergios said. “We dispense tax relief with an eyedropper—and expect families to navigate a maze of credits and deductions. For lower- and middle-income families, having to hire a tax professional to understand the maze of rules is just another kind of tax. They need broad-based relief.”

The report recommends doubling the Commonwealth’s personal exemption and indexing it to inflation, as several states have done. The study estimates that the change would reduce revenues by approximately $1.2 billion annually and could be phased in over several years to minimize fiscal disruptions. While it would not provide relief on the scale of the proposed ballot initiative, the reform would represent an important step toward broader, simpler, and more transparent tax relief.

The report also calls for a comprehensive review of the Commonwealth’s system of credits and deductions. Such a review would assess whether relief is being delivered broadly and effectively and compare Massachusetts’ approach with those of competing states to identify better ways to support working families.

About the Authors:

Jim Stergios is the Executive Director of Pioneer Institute, where he provides leadership in the strategic development of the organization, advancing its capacities and expanding its work in states across the nation. Prior to joining Pioneer, he served as Chief of Staff and Undersecretary for Policy in the Commonwealth’s Executive Office of Environmental Affairs, where he spearheaded efforts in water policy, regulatory reform, and urban revitalization. He has also founded and managed a business, taught at the university level, and served as headmaster at a preparatory school.

Aidan Enright is Pioneer’s Economic Research Associate. He previously served as a congressional intern with Senator Jack Reed and was a tutor in a Providence city school. Mr. Enright received a B.S. in Political Science and Economics from the College of Wooster.

About Pioneer Institute: Pioneer empowers Americans with choices and opportunities to live freely and thrive. Working with state policymakers, we use expert research, educational initiatives, legal action and coalition-building to advance human potential in four critical areas: K-12 Education, Health, Economic Opportunity, and American Civic Values.

Related Publications