June 30, 2026

Homeowners Insurance Premiums Continues to Rise Amid Climate Risk

Across the United States, annual homeowner insurance premiums have increased by an average of $648 from 2021 to 2024, according to the Consumer Federation of America. While there are widespread cost increases nationally, several communities have been hit harder than others due to the rise in severe weather events in the past few years. The states that saw the greatest percentage increase in premiums were Utah (59%), Illinois (50%), Arizona (48%), and Pennsylvania (44%). This contrasts with those states that saw the greatest hike in absolute dollars, which were Florida ($2,118), Louisiana ($1,775), and Kentucky ($1,426).

These two pieces of data tell us two things about the effect of climate risk on insurance premiums: new areas are being exposed to disasters and known high-risk areas are facing exacerbated impacts.

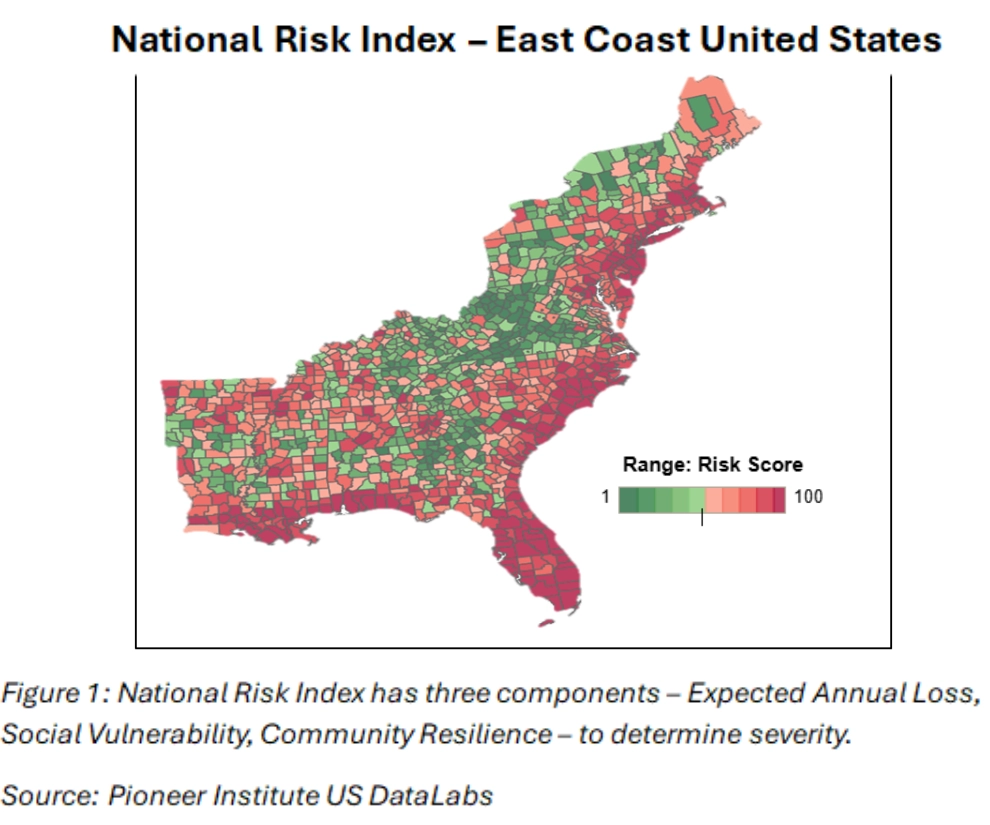

The map above illustrates how risk varies across the East and South, especially for some of the states where insurance premiums are increasing rapidly: Pennsylvania, Florida, Louisiana, and Kentucky. Areas like Florida and Louisiana experience high risk due to proximity to the coast and the associated susceptibility to flooding and hurricanes. However, it is not just high-risk states that are experiencing increases in premiums. Low- and middle-risk states have seen an uptick of almost 30% in their premiums on average.

For a middle-risk state like Kentucky, steep increases can be attributed to the rise in wind and hail events across the state and flooding from the Ohio River. Kentucky’s National Risk Index score is actually quite moderate; they score low-to-moderate in social vulnerability and high in community resilience. Since 2023, however, the dramatic increase in severe weather has driven a 34% increase in homeowner premiums, despite Kentucky exhibiting small losses in agricultural and building value, while the neighboring states of Ohio and West Viriginia have stayed constant.

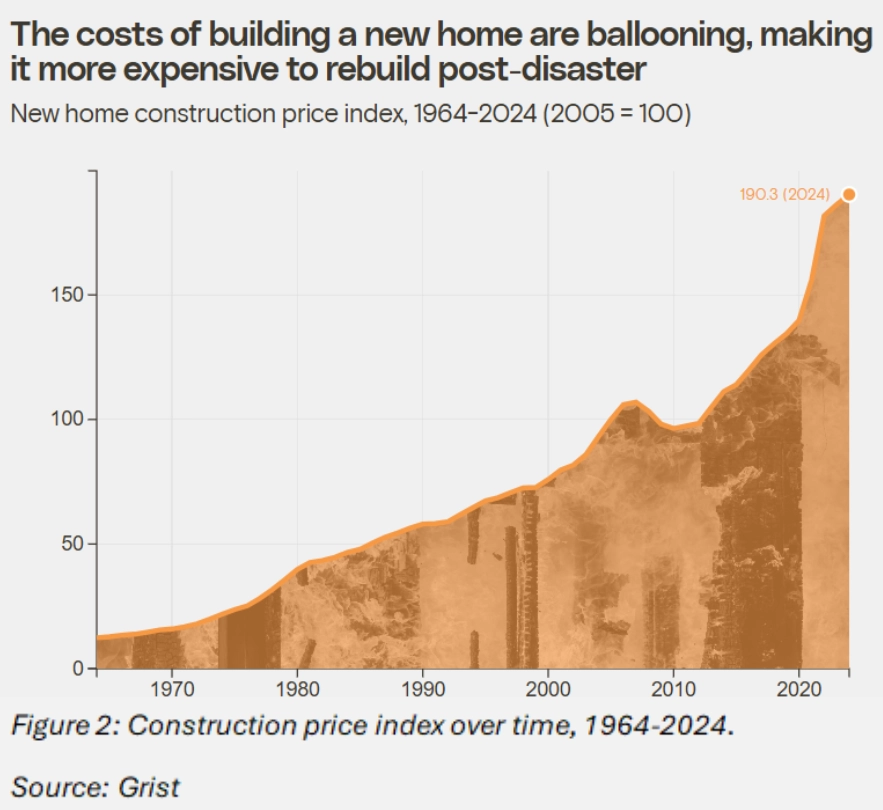

Higher premiums also stem from the way costs have skyrocketed in the years since the pandemic. Building materials and skilled labor costs directly influence housing prices, which indirectly impact insurance pricing as well. Because homeowners’ insurance covers the “replacement value” of homes, rising material costs can account for rising premiums. Insurers have argued that rate increases are also attributable to general inflation, but material costs have outpaced inflation since the pandemic. Above, Grist has calculated the construction price index to give a relative measure of how home construction prices have steadily increased since as early as the 2008 recession and accelerated in 2020.

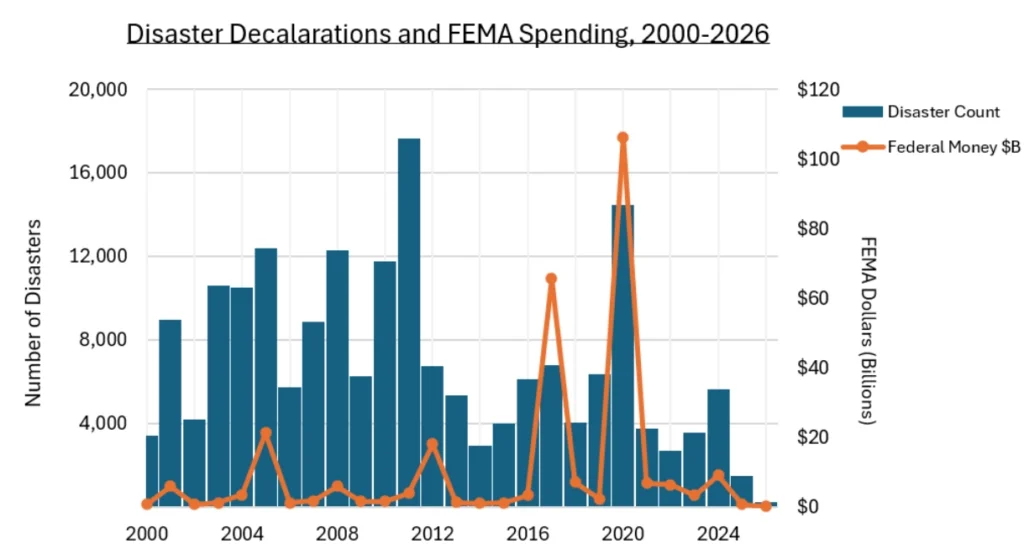

Figure 3: Number of disasters in comparison to dollars allocated through FEMA, 2000-2026. Source: Pioneer Institute US DataLabs

Homeowners can reduce their insurance premiums by maintaining good credit scores and avoiding risky additions to their property like swimming pools and trampolines. For events like natural disasters that are out of our control, the cost of rebuilding should be covered by insurance premiums and the help of federal programs like FEMA. Despite the rise in climate related incidents in the past decade, FEMA disaster declarations are limited to major weather events that do not encapsulate the full picture of response seen across the United States. Because of this, the federal government has cut approximately $750 million in resilience funding and taken back $900 million in allocated grant funding for preventative methods like stormwater systems, prescribed burns, and flood-control networks. The federal government has also reduced its staff by approximately half and raised the bar for what is defined as a FEMA level disaster response, putting the onus on the states and residents to manage the fallout. Figure 3 displays the reduced reporting of disasters in 2025 and 2026 as well as the steep reduction in federal dollars obligated to disasters.

With FEMA’s narrowed scope of disaster relief, states and local governments must prepare to take on more accountability for downstream costs that will inevitably fall to them. Expanding FEMA’s capacity to help prepare for the unexpected could be a reasonable way to mitigate the brunt of the costs falling on insured homeowners and already struggling states in the Gulf Coast and mid-Atlantic regions, where there are upwards of 200,000 applications for housing related assistance requested through FEMA’s Individuals and Households Program. If FEMA is limited in how much funding it can provide state and local governments, it can help states develop a timeline for taking over responsibility, as budgets in high-risk states will struggle to handle the need.

As FEMA narrows its role in disaster response and recovery efforts, state and local governments will be forced to shoulder a larger share of disaster-related costs. This shift will likely strain already struggling high-risk states, particularly those in the Gulf Coast and Mid-Atlantic regions, where more than 200,000 applicants have sought assistance through FEMA’s Individuals and Households Program. FEMA’s support of preventative measures and resilience efforts could reduce downstream costs for both taxpayers and local governments. If additional funding is not feasible in the long-term, FEMA should work with states to develop a timeline and strategy for taking on greater responsibility for managing disaster response to continue meeting residents’ needs.

Disasters and rising inflation are inevitable yet unpredictable. Planning around the risk could provide future relief despite the upfront costs.

Mia Raineri is a Roger Perry Government Transparency Intern at Pioneer Institute. She recently earned her M.S. in Applied Economics from Boston College.

Related Publications